Millions of Americans are channeling the classic Eagles tune Hotel California in their experience with student loan debt: “you can check out any time you like, but you can never leave.”

Two emergent trends encapsulate the inescapable trap of student debt repayment. First, the rate of serious delinquencies on student loans is approaching an all-time high. Second, student loan debts are intentionally made nearly impossible to discharge, even in bankruptcy.

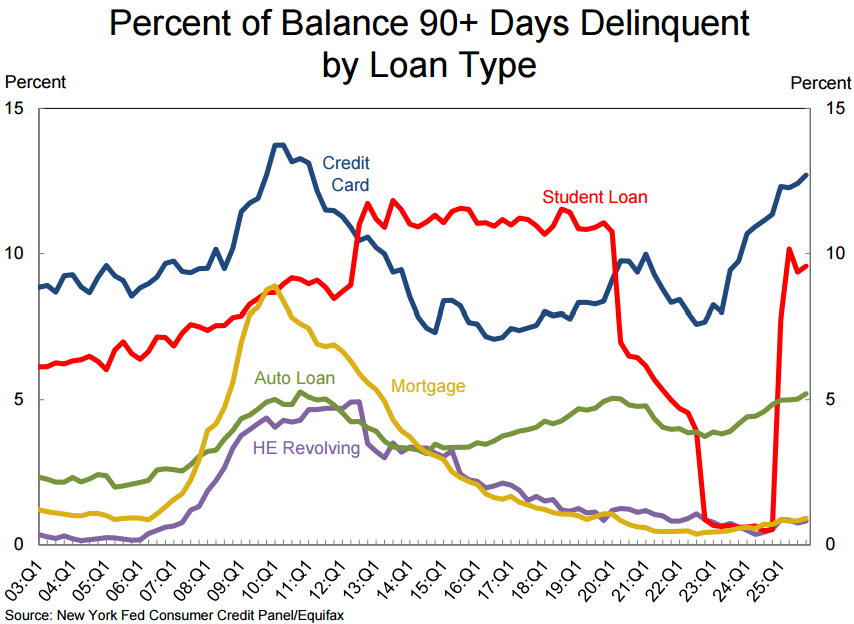

The Federal Reserve’s Quarterly Report on Household Debt and Credit has just been released, and it’s not a pretty picture. Alongside debt on student loans spiking, seriously delinquent (90+ days late) credit cards have reached levels not seen since the financial crisis. About one in eight credit card accounts is now three months behind. This trend has been rising since 2022, and seems to indicate that households were already beginning to fall behind on their debts, setting the stage for serious delinquencies.

Not to be outdone, auto loan serious delinquencies have also been on the rise since the beginning of 2023. Put these factors together, and it seems that the temporary COVID-era relief on student loan repayment didn’t make it any easier for borrowers to pay down their credit cards or car loans. In the meantime, serious delinquencies for mortgages are very low, but this is easily explained. With the ultra-low interest rates that many homeowners have on their mortgages, they stay put longer, overall saleable inventory declines, and home prices remain high despite the relative increase in interest rates since their pandemic-era nadir.

Combine all those factors, higher home and rent prices, greater reliance on credit cards, and increased reliance on longer term car loans (over 20 percent are now of the 84-month variety), and you wind up with a perfect storm to place additional pressure on student loan repayments. The backlash was waiting to be unleashed after a long period of genuine forbearance, along with an administrative shell-game that hid the seriousness of the fragility of the student loan market.

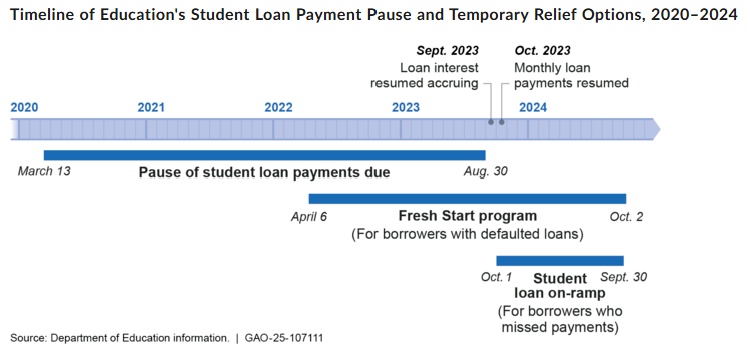

With the passage of the CARES Act in March of 2020, most federal student loan repayment was suspended, with no additional interest paid. Further, collections on defaulted loans were halted. These were supposed to have been temporary measures. Instead, they lasted until October of 2023. And even then, policymakers created a so-called “on-ramp”.

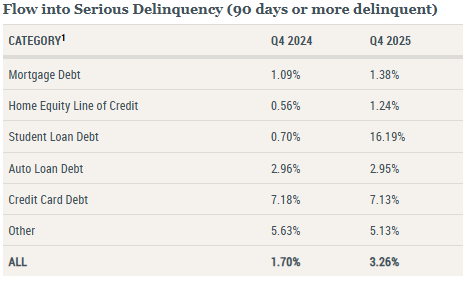

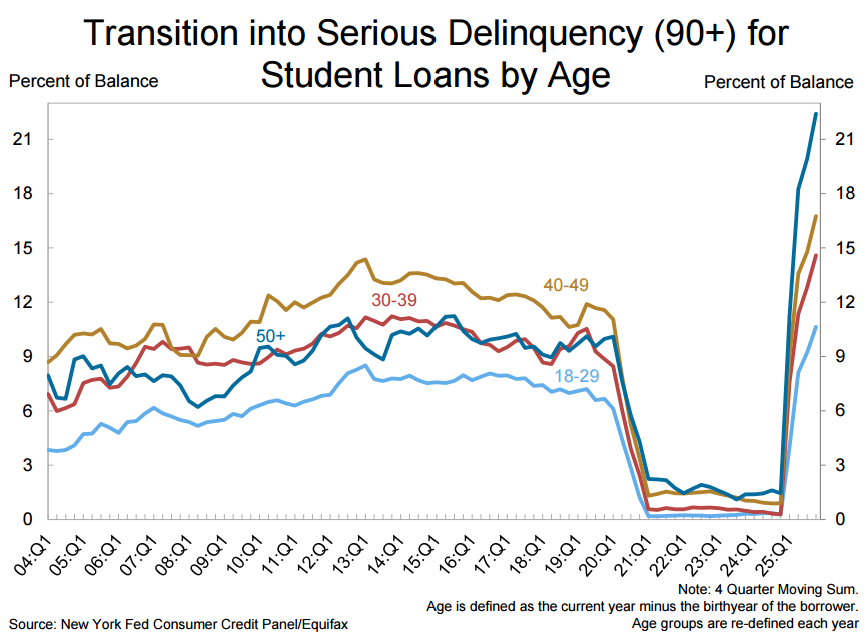

Amazingly, during that timeframe, missed payments were simply not reported. So, by the end of Q4 in 2024, only a paltry 0.7 percent of student loans (both federal and private) were sliding into serious delinquency. A year later, the real state of affairs became evident. The share of student loan balances that moved into serious delinquency shot up to 16.19 percent.

(Source: newyorkfed.org)

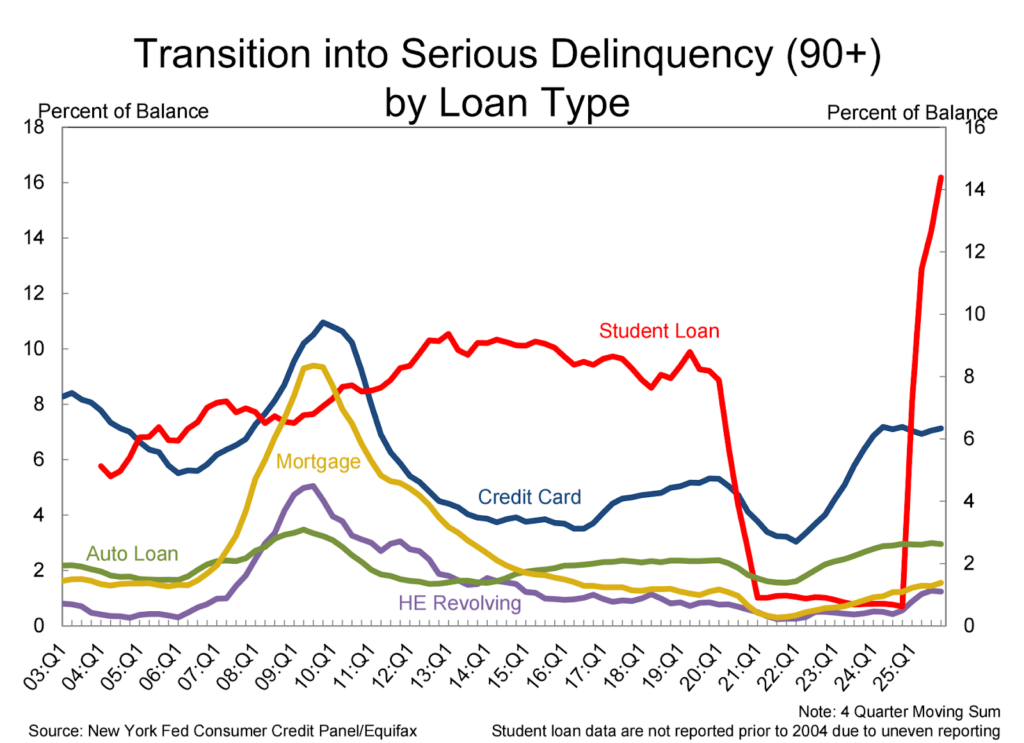

Of course, no trend lasts forever nor maintains the same pace, but new serious delinquencies in student loans have surged to levels not seen since the Fed began tracking this category in the early 2000s. With both credit card and car loan serious delinquencies on the rise at the same time, increased bankruptcy filings might be anticipated in the months ahead.

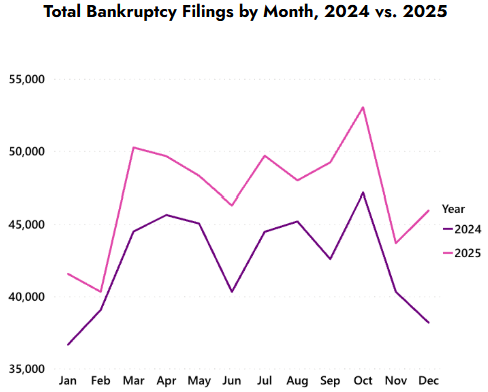

In fact, we don’t have to prognosticate on the future regarding bankruptcy filings. The American Bankruptcy Institute tracks all filing types, and every month of 2025 saw higher numbers of bankruptcies when compared with 2024. Last year saw a 12 percent increase in individual filing, coming in at 533,949 compared to 478,752 in 2024. And even within that window, each month of 2025 saw more bankruptcies than the year before.

If the same trend unfolds for 2026, it’s clear that the surging student loan crisis will have something to do with it. But here’s the problem for these borrowers: unlike many other forms of debt, student loans are the financial equivalent of Hotel California. Once you’re in, you can (almost) never get out.

Those inclined to look deeper can consult US Bankruptcy Code (Section 523(a)(8)) and the special privileges it gives to the student loan industry. In brief, this provision says that “student loans are not dischargeable unless it would impose ‘Undue hardship’ on the debtor.” How does one prove that they’re under undue hardship? In most US Circuit Courts, debtors have to prove to the court that their situation meets the infamous “Brunner Test”.

According to this legal standard, the debtor has to prove that:

- Repayment creates a hardship that would prevent a minimal standard of living

- The hardship is likely to continue

- The borrower has acted in “good faith” to try to repay

It doesn’t take a legal eagle to understand that each of these proof points relies on the subjective decision of a judge. Out of the 13 federal circuit courts, only two (the first and eighth) use what is called the “totality of the circumstances” standard, giving the court much greater latitude to discharge student loan debt. A year after those two courts adopted that standard, nearly every case went in favor of the borrower with some or all of their student loans being wiped away. But those wins were a tiny fraction of the nearly 43 million student loan debtors, who now owe a collective $1.66 trillion.

What may come as a great surprise to some is the age of borrowers falling farthest behind. For student loans (unlike car or credit cards), older borrowers led the surge in new serious delinquencies. More than 21 percent of borrowers over age 50 had their loans go 90+ days late at the end of 2025.

After all, it’s mainly Gen Xers — who could sing every lyric of Hotel California by heart — now discovering that, despite their best efforts, government intervention has made student loans nearly impossible to escape.

0 Comments