ESG has made significant inroads in the finance and investing community. Environmentalists have long used divestiture campaigns and impact investing to influence companies via finance. Their impact was relatively small and on the margins of financial markets. Today, they hope to make these activities central to finance.

Rather than simply trying to persuade individual asset managers to punish big polluters, ESG advocates want to rebuild the financial system around “sustainable finance” so that capital flows to firms advancing ESG goals and away from firms that don’t.

Their ideas have gained traction by arguing that ESG criteria can help companies assess and manage risk better, thereby improving profitability. But, in a classic bait and switch, companies tend to be scored not by their risk mitigation, but by whether they meet certain ESG parameters of emissions, renewable energy usage, diversity, stakeholder buy-in, and the like.

ESG “sustainability” finance falls into three buckets:

- Sustainability Debt Markets

- Sustainability Equity Markets

- Sustainability International Transfer Payments

Sustainability Debt Markets

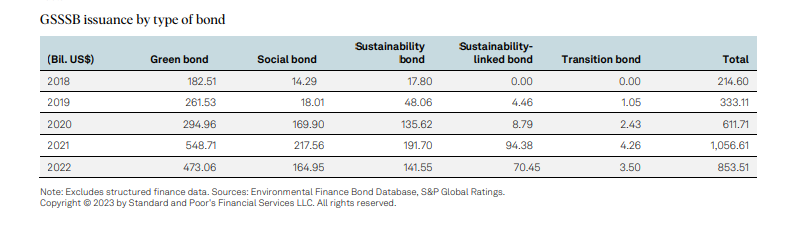

People use the label “sustainable” for bonds in the ESG debt market. But given the ESG movement’s penchant for acronyms, you may hear it described as the GSSSB (green, social, sustainable, and sustainability-linked bond) market. What counts and doesn’t count as a green bond, or a social bond, or a sustainable bond, can be a bit confusing, so our international finance overlords…I mean helpful, benevolent advisers…have given us some guidance.

Many organizations offer definitions and guidelines for whether certain activities qualify as “green” or “social” or “sustainable.” The most important is the “Taxonomy” created by the European Union:

The taxonomy provides a framework for assessing the degree to which an economic activity contributes to one or more of the EU’s six environmental objectives: climate change mitigation, climate change adaptation, sustainable use and protection of water and marine resources, transition to a circular economy, pollution prevention and control, and protection and restoration of biodiversity and ecosystems.

For a business to be classified as environmentally sustainable according to the taxonomy, it should fundamentally contribute to one or more of the six determined sustainability and environmental objectives, and at the same time not cause significant damage to any of the remaining objectives.

The Climate Bonds Initiative offers a slightly different taxonomy – same story, different slicing and dicing of approved criteria. Its Climate Bonds Standards offer guidelines and certifications of whether bonds meet selected ESG criteria.

The International Capital Market Association publishes many guides for sustainable debt issuance:

- Green Bond Principles, Sustainability Bond Guidelines, and Sustainability-Linked Bond Principles

- Climate Transition Finance Handbook

- Pre-Issuance Checklist for Social Bonds

- Social Bond Principles

The Pre-Issuance Checklist for Social Bonds and the Social Bond Principles sound like something out of the Soviet Politburo. One document literally states: “The SBP, and the Principles generally, are coordinated by the Executive Committee with the support of the Secretariat….”

- Green Bonds – money borrowed for projects that address climate change and/or improve local environments

- Blue Bonds – a recently created environmental bond subcategory focusing on water-related projects. The Asian Development Bank says these projects: “Conserve and restore critical marine habitats and species,” “reduce marine pollution,” and “grow blue economies.”

- Social Bonds – money borrowed for projects that advance some social goal

- Gender Bonds – money borrowed for projects that fund and advance women

- Racial Equity Bonds – money borrowed for projects funding minority communities

- Sustainability Bonds – money borrowed to advance both environmental and social goals

To summarize, “Green” or “Blue” bonds refer to borrowing that supports various environmental goals – renewable energy production, greenhouse gas mitigation, or ecosystem protection and preservation for example. “Social” bonds refer to projects that advance some social priority like affordable housing, food security, or advancing gender or racial equity.

The total issuance of green bonds has surpassed $2 trillion dollars, with almost $450 billion being issued in 2023. According to Statista, $582 billion dollars of green bonds were issued in 2021 and $487 billion were issued in 2022. When you add other kinds of sustainability bonds, over a trillion dollars worth were issued in 2021, and close to a trillion dollars were issued in 2023.

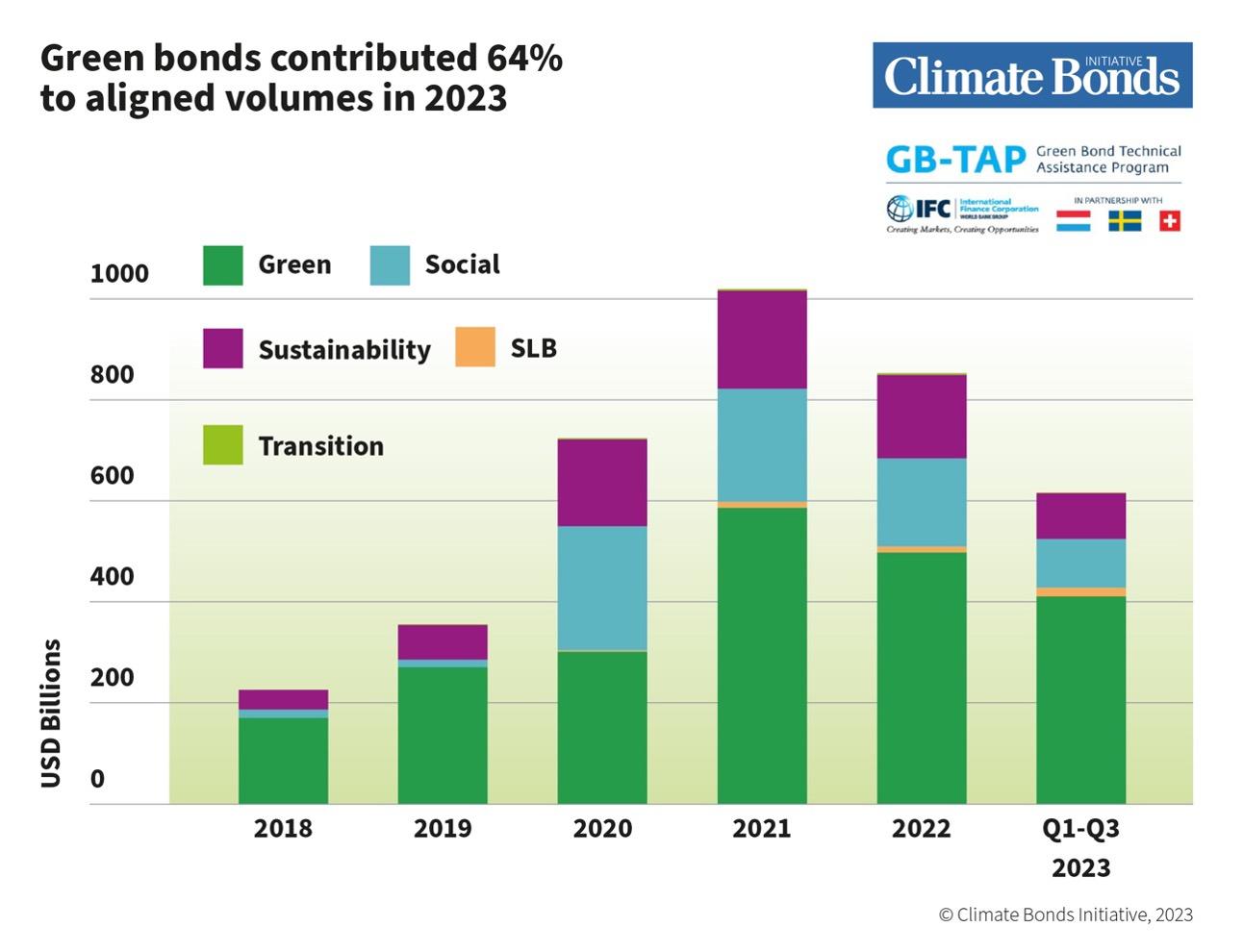

The Climate Bonds Initiative gives an interesting breakdown of the largest projects by region, country, and company across green, social, sustainable, and sustainability-linked projects. They also show the overall proportions of different kinds of sustainability bonds issued globally:

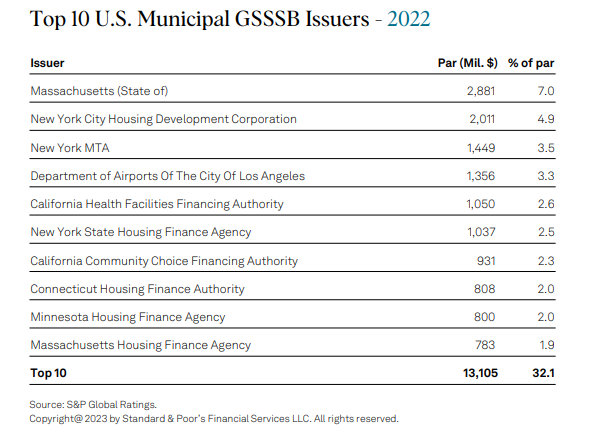

US municipalities, especially in California and New York, represent one of the fastest-growing areas of sustainable debt (green, social, and sustainability bonds). They issued $27 billion in 2020, $46 billion in 2021, and at least one forecast of $54 billion in 2023.

GSSS bond issuance by US municipalities has averaged about $40 billion per year over the past three years. It has risen to over 10 percent of total municipal borrowing, and will likely surpass 12 or even 14 percent of total municipal borrowing in the next twelve months. The proportion of green bonds issued by municipalities has declined relative to social bonds as various state housing agencies have begun aggressively issuing social bonds to fund their various projects.

Here are the top ten municipal issuers of Sustainable bonds in 2022:

Sustainability Equity Markets

Various brokerage firms and institutional investment managers have offered funds labeled ESG for years. A great deal of controversy has dogged this part of the market. What firms qualify for ESG selection? It depends. How different are “ESG” index funds versus regular index funds? It depends, but they are usually not very different. What kinds of returns do ESG funds see relative to other funds? It depends, though after including fees the returns seem to be lower.

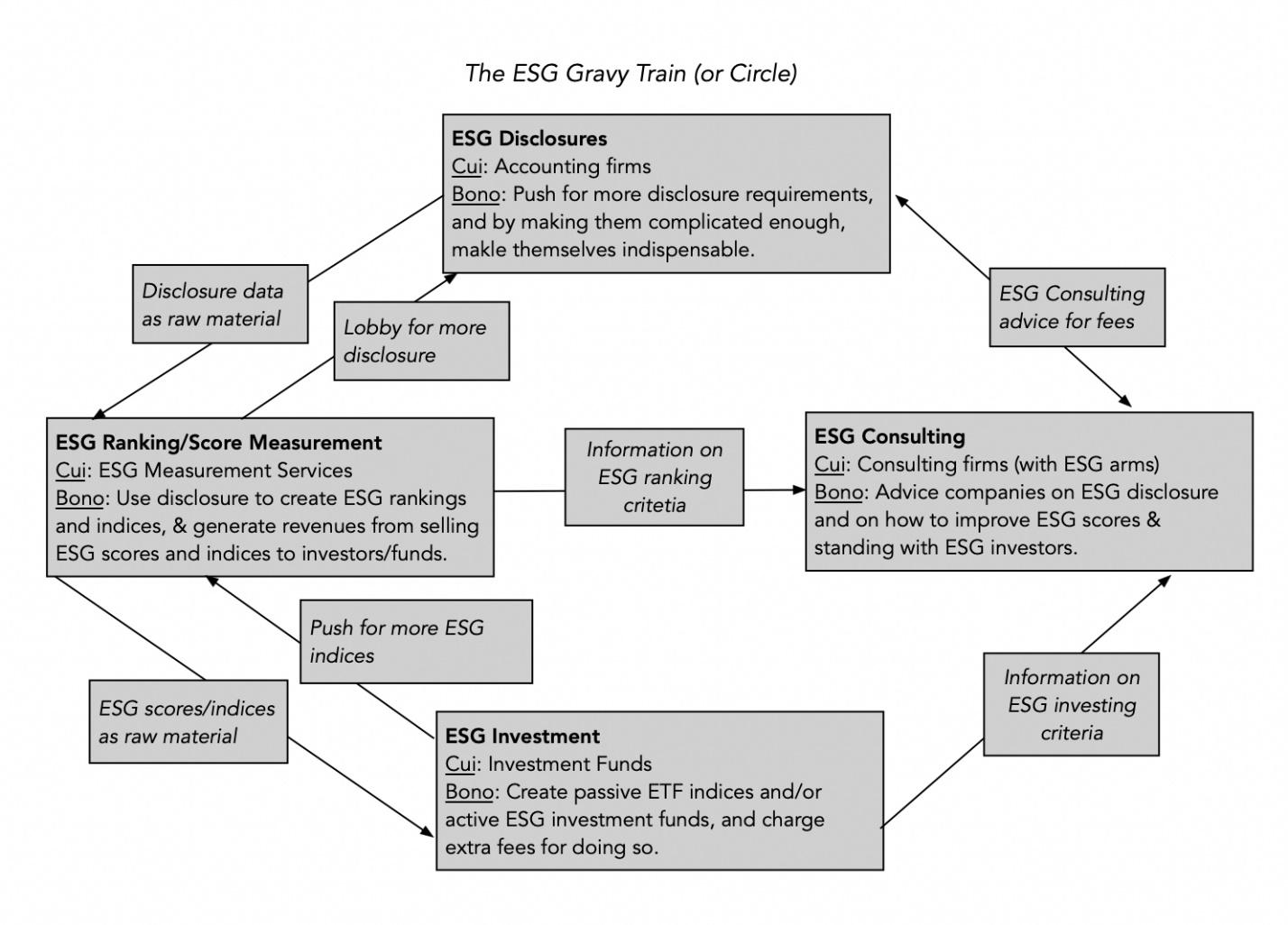

What is clear, though, is that many participants in the process of creating these ratings and funds benefit financially. NYU professor Aswath Damodaran created the following diagram to illustrate which firms benefit from the growth of ESG or Sustainable finance:

The ambiguity around ESG ratings and the composition of ESG funds make judging impact and scale difficult. Trillions of dollars are invested in ESG-related equities, yet much of that goes towards companies that regular indices hold (tech stocks, financial stocks, etc.). Often ESG investment in equities simply validates what companies are already doing.

Apple and other large tech companies, for example, have long actively promoted ESG types of activity. But these companies engaged in these activities before there was much benefit to be had through ESG finance. And they are likely to continue in these activities even if ESG finance no longer offers them much benefit. It seems doubtful that ESG investing has changed that much.

But ESG finance does give tremendous power to ratings agencies. They can reward companies, like ExxonMobil, that move in a direction they like while punishing companies, like Tesla, whose executives they dislike. What ends up mattering for many companies when it comes to sustainable-equity finance is not improving their scores, but making sure they score high enough to be in ESG index funds.

If the threshold for ESG designation is a score of 58 (hypothetically), it is far more beneficial for a company to increase its score from 55 to 60 than from 60 to 90 – even though from an impact standpoint, the latter theoretically represents a much larger increase.

ESG considerations represent a mainstreaming of “impact investing” while giving “fiduciary” cover to large institutional investors who invest trillions of dollars of other people’s money in ways that advance mostly political priorities.

Sustainability International Transfer Payments

Climate Finance refers to large-scale lending and financing of “transition” projects in developing countries. It is very similar to the criteria for green bonds, except in these cases the repayment, or loan principal, is held in the form of discrete loans rather than bonds. The push internationally is for countries to increase their commitments to making these kinds of loans through the World Bank and the International Monetary Fund. There is also a push to get private banks and investors to match government fund contributions towards climate finance.

These investments are called Just Energy Transition Projects (JETPs). These projects were first created after COP28, with several countries backing funding for South Africa. Only a few JETPs have been created since then, such as $20 billion for several related green energy projects in Indonesia, or more recently a one billion dollar loan program between South Africa and the UK. Although not many of these projects have been finalized, many are in the works and the participants in COP28 (and the previous two conferences) have signaled that these kinds of projects will be an important part of the transition to lower-carbon emissions.

In 2022, climate activists proposed the creation of a global Loss and Damage Fund. The fund would pay for losses or damage that countries experience due to climate change. Videos like “How Can You Flee Climate Change” by the United Nations High Commissioner for Refugees (UNHCR) encapsulate the reasoning behind creating this Fund. Wars, floods, droughts, snowstorms, and other natural disasters in poor, rural communities are highlighted as problems resulting from climate change. Wealthier countries that have produced significantly more emissions than developing countries have over the last 100-200 years are supposed to compensate poorer countries for the damage they experience due to climate change – floods, droughts, heat waves, and the like.

At the annual climate conference in 2023 (COP28), an agreement was made to set up the Loss and Damage Fund with voluntary contributions from developed nations. The initial commitments add up to very little; about $700 million in pledges when they want around $400 billion per year to “compensate” the governments of poorer countries. One of the predictable sticking points was whether China and India ought to contribute to the Fund or receive compensation from it.

Conclusion

ESG finance is a pervasive, rapidly growing field spanning debt issuance and equity finance to massive international lending and grant programs. While the goal on much of the private side of ESG finance involves steering companies towards making decisions to advance ESG priorities, on the government side the goal appears to be funneling money from wealthier countries to poorer countries. From a dollar standpoint, far more money is being lent from wealthy countries to developing countries for climate projects than is being given away. But it remains unclear how much ESG advocates of the wealth transfers between countries want the aid to revolve around humanitarian relief or “climate compensation” versus how much they want the aid to revolve around financing “de-carbonizing” the economies of those countries.

The least-known, but potentially greatest, impact of ESG finance in the US comes from the municipal bond market. There appears to be significant growth in the absolute and relative quantity of municipal bonds being issued as GSSS bonds. Over time, issuing such bonds will come with more and more strings attached to the projects being funded, whether for housing or infrastructure or schools.

Understanding the dimensions of ESG finance, especially in the US municipal bond markets, and the goals of ESG advocates, should make us more curious and skeptical when local school boards or townships ask the public to authorize new debt issuance. We should care about whether such bonds will be issued with the label “sustainability” and all the strings that come attached.

0 Comments