In his new book The Fiat Standard, it’s clear that Saifedean Ammous thinks all bad things come from the government. Specifically, everything wrong in American life stems from the money-printing that is under the government’s control.

To Saifedean, or Saif as his followers call him, Fiat means something more than a monetary system backed by nothing but a nation state’s promise to steward it well. He equates Fiat with centralized Big-Government control and a runaway belief that lots of Nice Things can be had by flick of a wand (considering some characters in governments, that’s not entirely unbelievable).

Further, everyone, according to Saif, is on the Federal Reserve’s payroll, or is somehow a beneficiary of its “infinite credit line.” Even the International Monetary Fund is not safe, which seems strange given that it runs its own unit-of-account currency (Special Drawing Rights).*

Throughout the 350-page rant that is The Fiat Standard, Saif repeatedly comes back to the recipients of government-money-from-nowhere. He claims schools are broken because they have an infinite supply of fiat money at their disposal and teachers on fiat salaries destroy education; higher education and scientific research are broken because they rely on an endless supply of government grants, enabled by fiat money, which results in botched research.

Finally, he targets the development industry, which he claims is filled with miseducated economists with degrees from what he describes as “Keynesian and socialist fiat universities.” Going further, he claims these economists have access to “a line of credit from the Federal Reserve [which] grants them immunity from market failure.”

Everything that’s broken receives fiat money, with the implication that fiat is the reason they’re broken. But where does fiat money really come from? And are all these institutions and their bureaucrats really funded by their central banks?

Saif explains that

modern fiat money is not conjured out of thin air through government fiat. Governments do not just print currencies and hand them out to societies that accept them as good money.

Well, the Fed’s open-market purchases are conjured out of thin air by decree (i.e. government “fiat”), and that’s the base layer of our money – the concept economics textbooks used to call “high-powered money.” The vast majority of outstanding fiat, Saif explains, is digital, created through commercial banks issuing debt. The benefits to the people involved are clear: the home buyer doesn’t have to save up before purchase; the homeowner can sell to a larger range of people and get a higher price; and the buyer pays the bank interest for decades to come. Everybody wins in this story – except the current money-holders whose holding gets diluted by the new money.

To the extent that this description is accurate, the parties to this money creation process have this in common: Their purchasing power isn’t the government’s to spend. It’s the homeowner who receives the new money and spends it, and it’s the banks profiting from the interest rate they charge the borrower. This raises the following question: Where’s the government benefit that it can so freely dispose of, all those infinite credit lines and fiat money that fuel the world’s stupidity?

Quantitatively Speaking, Where’s My Fiat?

The problem emerges again and again, as Saif isn’t bothered by pesky distinctions between various parts of government, and therefore thinks of the central bank’s money-printing ability as the same as the Treasury’s spending ability. Economically and historically speaking – and ironically, MMT-speaking – he’s not entirely wrong: Every episode of hyperinflation has seen fiscal powers subdue whatever level of independence the monetary powers may have once had or resistance they might have put up. But what every episode of hyperinflation also shows is that there’s a limit to how many real resources the government can extract through inflation. The monetary authority may decide the base money supply, but the public decides its real value. As Scott Sumner writes, and many other monetary economists have pointed out,

The Fed controls the nominal quantity of money in the US economy. If it wants to increase the money supply, there’s nothing the public can do about it. Unless people want to burn the new money in their fireplaces, they must hold these increased cash balances. [B]ut the public determines the real demand for money.

Monetary economists and historians sometimes speak of “Seigniorage,” the spread between the cost of producing new money and the purchasing power that the money has. Most countries don’t maximize their seigniorage revenue, precisely because of the political backlash that accompany such extractive inflation regimes.

Under digital fiat regimes, we usually think of this revenue as the interest income on assets corresponding to the portion of the central bank’s liabilities that it doesn’t have to pay interest on. For the US, that’s whatever the $2.2 trillion or so of dollars circulating is financing – giving the Fed an interest-free financing of about a quarter of its soon-to-be $9 trillion asset portfolio. At maturity-weighted yields on its portfolio of Treasuries and mortgage-backed securities, that’s somewhere north of $100 billion a year.

As seen in the remittance that the Fed sends to the Treasury every year ($54.9 billion in 2019, $88.5 billion in 2020, $107.4 billion in 2021), the Fed’s operations do directly cover some government expenditures – in the range of around 1 percent of outlays:

Until 2019, the US public sector spent some 39 percent of GDP – putting it in the lower half of OECD countries. Right off the bat, then, there’s a problem with thinking that the Federal Reserve’s money printer finances the government’s expenditures; their vast numbers don’t add up. Over $100 billion in direct funding is not nothing, obviously, but it’s far from the free-for-all money spree that Fed critics like Saif sometimes imagine.

Granting him some linguistic leeway, “government money printers” or “access to an infinite credit printer” doesn’t seem to cut it either. Where exactly is this endless limitless pool of funds with which fiat provides government?

During certain periods in the pandemic the Fed’s purchases on the open market amounted to a large share of the bonds newly issued by the US government, leading to indignant calls that the Fed is now clearly monetizing government spending. Put in context, over a longer time frame (and not specific markets like TIPS), that looks less compelling:

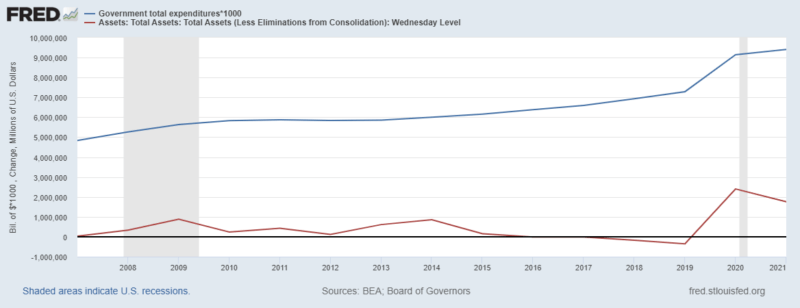

This is the federal government’s expenditures (in millions) and the yearly increases in the Fed’s balance sheet (also in millions). You can read the red line as the increase in new money stemming from the Fed – as a flow rather than a stock indicator, becoming directly comparable to the government’s annual expenditures. Importantly, that money does not accrue to the government: While it’s misleading to say that the Fed’s open-market purchases finance the government’s spending outright, the Fed is adding buying pressure to the bond market that does.

Even though the Fed backstops government debt markets, implicitly and explicitly, it’s overwhelmingly clear that government spending is much, much larger than that. To say that fiat printing is the reason the government spends so much misses the taxation elephant in the room.

The question remains: Where is all the supposed money coming from?

One answer could be a hypothetical argument from nowhere, that is that absent soft money, the US government would pay much more on its debt, which would make deficits costly, thus forcing the state to become smaller (and a smaller one wouldn’t, somehow, distort schooling or science or architecture etc). The mechanism certainly holds. Should the Fed, as one of the largest buyers on the secondary bond market, suddenly disappear, the effect would be market rates on US Treasuries rising. But by how much? And would it be enough to turn the trillion-dollar taxation leviathan into whatever size that the Saifedeans of the world no longer think is sufficiently small to avoid ruining the sciences or public morals?

Even still, the US government manages to raise tax revenue to the tune of $4 trillion a year, almost the full extent of the Fed’s balance sheet increase from August 2019 until February 2022. Even if all the Fed’s balance-sheet increase were at the disposal of the government – which it’s not – it wouldn’t explain the many recipients that Saif believes are on the fiat-government payroll. Is there a cascading benefit of Cantillon effects, where the first recipients of new money benefit disproportionately to latter receivers? Possibly, but in comparison it would be quite limited. Show us the smoking gun, please.

A similar mechanism is the store-of-value argument – the monetization of assets like Treasuries, stocks, and real estate when we live under a bad monetary regime. In the absence of hard money, Treasuries have become the second-best safe asset. That additional demand, over and above what a hypothetical world of investors and savers would want to hold, lets the US government run bigger deficits at smaller costs.

Again, the mechanism is correct and has been a source of controversy at least since the “Exorbitant privilege” accusation from a French finance minister in the 1960s. But how large is that effect? And where is the compelling evidence for it that validates Saifedean’s harsh words?

There’s plenty wrong with central banking, no doubt, but showering broken institutions with infinite credit lines and opportunity-cost free funding isn’t one of them.

* It is well supplied by the member governments of the world (not, as Saif claims, their central banks). The IMF does report emergency credit lines, but from the US Treasury and not the Fed – and the largest provider is Japan, with the US share of IMF’s credit line commitment only 16 percent of the total (and the US is entirely absent from the bilateral government/central bank guarantees).

0 Comments