The biggest short squeeze I ever saw up front took place around Thanksgiving 1999. Interesting (and bad) things often occur at such times in financial markets: the senior (read: experienced) traders are off the trading desks, liquidity dries up, and ripples become tsunamis.

Before this introduction gets out of hand, a short squeeze is

an unusual condition that triggers rapidly rising prices in a stock or other tradable security. For a short squeeze to occur, the security must have an unusual degree of short sellers holding positions in it. The short squeeze begins when the price jumps higher unexpectedly. The condition plays out as a significant measure of the short sellers coincidentally decid[ing] to cut losses and exit their positions.

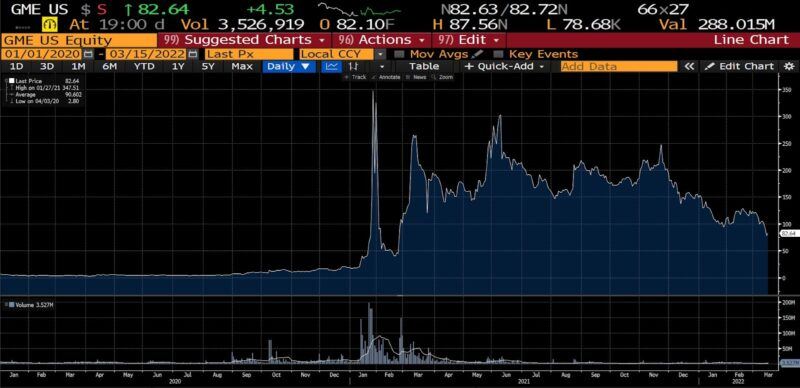

Although it’s a somewhat obscure topic outside of financial markets, the concept has become more widely known in public discourse since, early in 2021, a handful of ho-hum, low volume (and hence low liquidity) stocks were investigated by a number of Reddit communities, most notably wallstreetbets. When the groups determined that the stocks (including GameStop and AMC) had disproportionately massive short positions, they organized and began buying. In the panicked rush to escape rapidly losing positions, the short sellers had to buy frenetically, pushing prices even higher. And thus it was that GameStop ran from less than $20 per share to almost $350 per share in ten days.

GameStop stock price (2020 – present)

At the time, I attributed the behavior on both the institutional and retail sides to profoundly skewed risk appetites owing to a torrent of fiscal and monetary programs throughout the pandemic.

Ariel, 1999

So back to my story: The company was Ariel Corporation. This was during the dot-com era, so many were the attempts by firms to link themselves to the internet frenzy, whether or not that association was legitimate. In August of 1999 Ariel had traded as low as $1.50 per share at negligible volume. The company announced that, despite reliably losing money for years, it had been approved by certain government entities to produce modem cards for internet access providers. And so on a week where experienced traders were at home, preoccupied with turkey, stuffing, and cranberry sauce, the stock began rising. It inched up to $5 per share, spiked over $6, then fell back to between $4 and $5 per share. And then, it began to climb.

First, to $7, which excited a lot of younger and less experienced traders back on their desks. Envisioning a fall back to $4, they sold the stock short. At $5 and $6, they sold more stock short. At the price crossed $7 per share, still more was sold short.

On November 23, 1999, the day before Thanksgiving, the stock spiked from just over $7 to nearly $11 per share. At this point the stock appeared on the radar of opportunistic retail traders, hedge funds, and proprietary trading shops. All began jumping in, and the short position grew. In all, how many shares were shorted? Tens of thousands, hundreds of thousands, millions of shares? All waiting for Ariel Corp stock to go back to its rightful place, in their eyes: back down to $2 per share or lower.

Then came Thanksgiving. And for the record, Ariel did eventually trade below $2 per share, on July 28, 2000. But first came Friday, November 26, 1999.

I was not short (fortunately), nor was I long (probably also fortunately). But from the trading desk that day, amid the thin liquidity that characterizes days like the forlorn, ritually understaffed, post-Thanksgiving Friday, I watched nearly every tick as Ariel Corp rose to $15 per share. And then to $20. Then, accelerating, to $25, $30, $35, and above in an incredible, mounting hysteria. At one point I’m sure I saw a print at over $50 per share, but who knows? Officially, which is to say in terms of the data that we have today, on that day a stock which had for years traded less than 100,000 shares per day–sometimes much less–traded over 50 million shares, rising to $37 per share.

Ariel Corporation stock price (1999)

The message boards erupted shortly after 4pm that Friday. Rumors flew: that untold numbers of retail day traders were ruined; that a brokerage firm or two were in trouble; that this trader at that firm was “actually” long thousands of shares at $7 or $10 and rode them up, selling right at the top. Some scuttlebutt, of course, is more credible than others. What wasn’t speculative, however, is that the average size of an order in Ariel that day was 379 shares. As short sellers’ losses mounted, they sprinted into the market to purchase stock back at successively higher prices, drawing in other losing short sellers. And the stock of Ariel Corporation, a company which hadn’t made a profit since it began trading publicly in 1995, vaulted 410 percent in two sessions. It was delisted in 2010.

Nickel, 2022

The world some 8,123 days later was in many ways unrecognizable from that which prevailed in late November of 1999. Yet it was about to diverge even further from the past. Russian infantry, armor, artillery, and rocket units which had massed on Ukraine’s eastern border for months finally swarmed across the border, brutally seizing urban areas on their way west to capture Kyiv.

Russia has a relatively small economy, but it deals pivotally in a number of commodities which are absolutely critical to modern life. Oil, natural gas, and grains are among them. Nickel is also among them, although it rarely gets as much attention as platinum, palladium, copper, aluminum, gold, and most others. About 20 percent of the world’s nickel comes from Russia, and is used in making stainless steel, alloys, plating, and other uses (including batteries for electric cars). When Western nations around the world unleashed a deluge of financial sanctions against the Kremlin in response to the brutal attack on Ukraine, markets seized up. Individuals requiring a regular supply of physical commodities including oil, natural gas, grains, and nickel (among others), rushed into futures markets, buying to lock in prices for future delivery.

As early as February 22nd, nickel futures had risen to $25,000 per ton, the highest price since 2011. On March 1, 2022, the EU announced that it would ban a number of Russian banks from accessing the SWIFT international payments by March 12th, other than for energy transactions. In anticipation of scarcity owing to both being blocked from SWIFT and concerns regarding the security of shipping on the Black Sea, futures contracts burst upward.

Over the rest of the week, the 3-month nickel contract (in metric tons) on the London Metal Exchange (LME) surged 19 percent. And on Monday, March 7, 2022 the price soared 82 percent to the highest price ever in its nearly four-decade trading history: $52,700 per metric ton.

And then, not circumstantially unlike a quiet November Friday nearly 23 years earlier, the nickel market exploded upward. From the $48,000 per ton opening price on March 8th over the next 18 minutes the metal futures contracts sawtoothed violently up to over $100,000 per ton. It was an estimated 40 standard deviation move in price, which brought the 24-hour price change to roughly 250 percent. It also led the London Metal Exchange to close the market and break some 5,000 trades which had already been executed.

London Metal Exchange Nickel 3-month contract (2017 – present)

In futures contracts, for each long position there is a short position. And so trading in futures contracts (and in options), unlike in stocks and other securities, is in fact a zero-sum game on a contract-by-contract basis: A profitable move up in a contract is a loss for the short seller on the other side. As was soon discovered, the March 8th chaos was in part a short squeeze triggered by a Chinese tycoon named Xiang Guangda, and sometimes dubbed “Big Shot.” Xiang is the owner of the world’s largest producer of stainless steel and refined nickel, Tsingshan Holding Group.

Like so many other commodities, nickel production was leveled as global lockdowns and stay-at-home orders were put in place in the first quarter of 2020. As I described in the context of criminal syndicates organizing international catalytic converter-harvesting operations,

[a] large part of palladium’s scarcity derives from the fact that it is not, or at least very rarely, mined directly: the metal is typically found as a side product of nickel mining … In the spring of 2020, with Covid making its initial global march, many nickel and platinum mines closed entirely or reduced their labor force to skeleton crews. South Africa, which accounts for 36 percent of the world’s annual palladium sourcing and 78 percent of the world’s platinum, shut down mines on March 27th, 2020 for six weeks.

Did Covid mitigation policies, to some extent or another, precipitate the nickel tumult? Yes, but peripherally, according to Jack Farchy, Alfred Cang, and Mark Burton.

The seeds of the epic short squeeze were sown last year, when nickel, like all commodities, was rallying from its Covid-era low. Xiang didn’t believe the rally would last. He started increasing his short position on the London Metal Exchange … Why bet against nickel when you have a nickel business? Xiang wanted to increase Tsiangshan’s production dramatically by producing so-called nickel matte for electric vehicle batteries. The company had plans to produce 850,000 tons of nickel in 2022, an increase of 40 percent in a year, according to a person briefed on them … Everything changed when Russia invaded Ukraine.

When the LME nickel contract crossed $50,000 per metric ton on March 7th, several firms and funds received margin calls approaching $1 billion. Tsingshan’s margin calls were estimated to amount to nearly $3 billion. In the short 18 minutes that it took the nickel contract’s price to double on March 8th–some of which, propelled by Tsingshan’s traders desperately attempting to buy their short positions back at higher prices–the paper loss is thought to have exceeded $8 billion.

Xiang Guangda – “Big Shot” – and his Tsingshan Holding Group were negotiating a bailout throughout the 10th and 11th of March. Those discussions hit snags when the impaired nickel trader indicated his intention to pay the margin calls with rescue loans, but not liquidate his short position. Yesterday, on March 14th, several news sources indicated that a deal had been reached, and that there were more wrinkles to this story than a cheap suit with prunes stuffed into every pocket.

JP Morgan…[has] reached a deal to bail out the Chinese tycoon which is also its biggest nickel short counterparty. While by now most are probably tired of the neverending nickel saga on the LME, which has been exposed as a joke of a market catering to whale Chinese clients to avoid angering its Hong Kong (read China) owners…Tsingshan has reached an agreement with a consortium of…bank creditors on a standstill agreement.

The LME nickel contract, suspended since March 11th, will resume trading at 8am Wednesday morning in London, 3am EDT. In the interim the exchange has introduced a new daily trading limit: +/- 5 percent limit from the previous day’s closing price. While that essentially prevents the events of the first two weeks of March 2022 from ever occurring again, many of the regular metal traders are disgusted, deriding the LME as the Soviet Metal Exchange.

In a series of posts on Twitter, Clifford Asness, founder of [the $140 billion dollar fund AQR], described the LME as “slimeballs.” This was, he said, the first time he had been told “you don’t get your legitimate profits because, gee, someone else, a broker who didn’t manage things so well, might suffer.” “I’m accusing you [the LME] of reversing trades to save your favored cronies and robbing your non-crony customers,” he went on. The LME denied that parent company Hong Kong Exchanges and Clearing had influenced its decision.

As mentioned, when nickel resumes trading (six or seven hours from when this is being written) trading limits will keep prices from plummeting or skyrocketing as they might have otherwise. Meanwhile, prices of a handful of other critical metals–aluminum, notably–began moving more pronouncedly last week. Whether that was due to shifting financial circumstances behind broad-based commodity trading firms as nickel spun out of control, concerns about the Russo-Ukraine War, or both is unknowable.

London Metal Exchange Aluminum 3-month contract (2020 – present)

The Ariel squeeze came and went of its own accord in market-based exchange. Artificial fetters on the nickel market may arrest volatility for the time being, but will mute the clamant information conveyed in wartime price signals. Would, rather than closing the market, the LME’s allowing the nickel per ton price to have shot to $150,000 have induced a groundswell of new nickel sources to come into the market? Might it have inspired a global assessment of potential substitutes? Or might it have performed the considerably salubrious task of driving the most careless/reckless/unlucky institutional global commodity trader(s) into economic oblivion?

Whether or to what extent any of that matters–because it may not–depends to a large degree upon the prosecution of the war, and especially how long the hostilities endure. But two lessons loom unavoidably on the selvage. Securities and derivative exchanges are woefully far from free markets, worst of all when unrestrained pricing is needed most. And once again, the increasingly distant tendrils of pandemic policies are disrupting the present order, two years on.

Post-script: At 3am EDT, nickel contracts reopened on the London Metals Exchange after being halted for a week. Three contracts were bid, 8,600 were offered for sale. The market immediately fell 5%, and trading was halted again. The debacle persists.

0 Comments