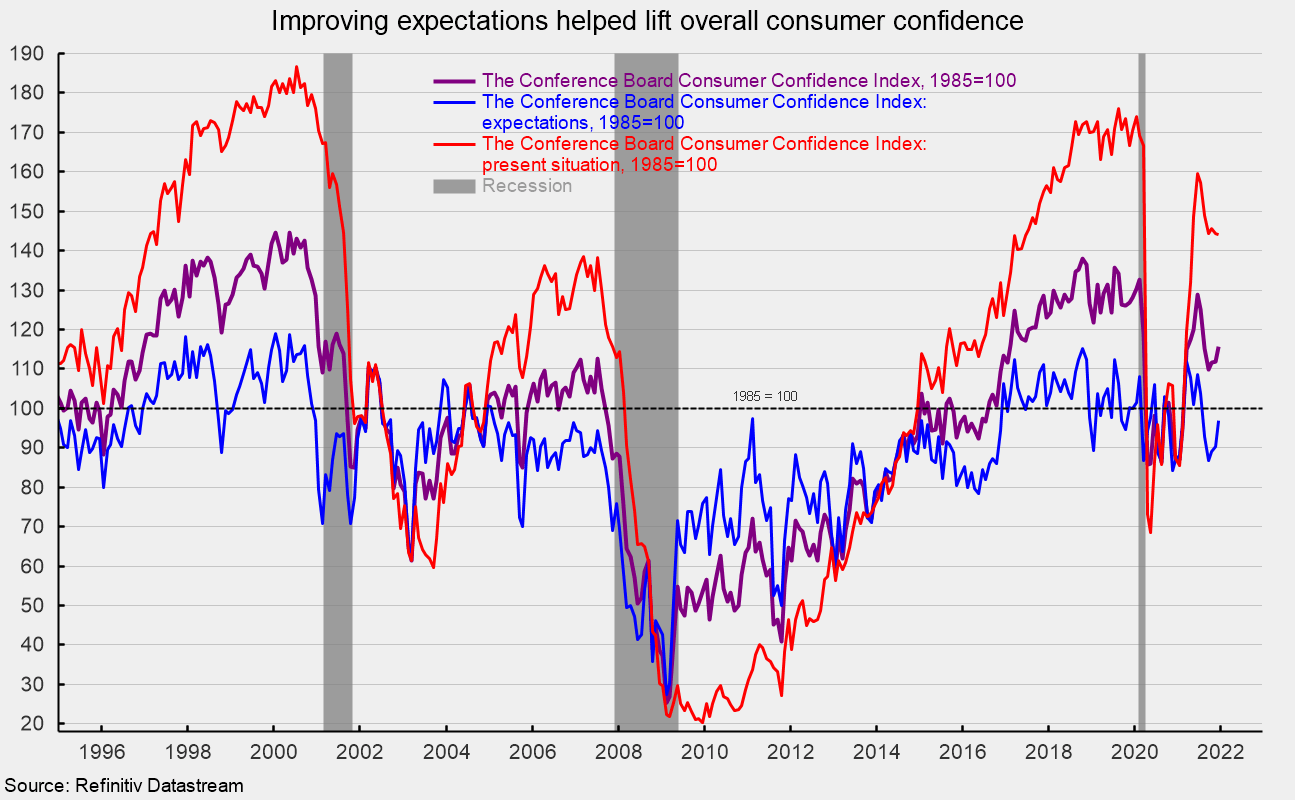

The Consumer Confidence Index from The Conference Board rose in December but remains at a historically moderate level overall. The composite index increased 3.9 points or 3.5 percent to 115.8 (see first chart). From a year ago, the index is up 33.0 percent.

The gain in the composite index was driven by the expectations component. The expectations component added 6.7 points, taking it to 96.9 while the present-situation component decreased 0.3 points to 144.1 (see first chart). The total index and both components remain well above typical recession lows but also remain below record highs. It should be noted that the data was collected before December 16 and may not fully reflect the rapid surge in new Covid cases due to the Omicron variant.

Within the expectations index, expected business conditions, employment conditions, and buying plans all had improvements while the expected income index fell slightly. For the present situation index, current business conditions improved while employment conditions weakened.

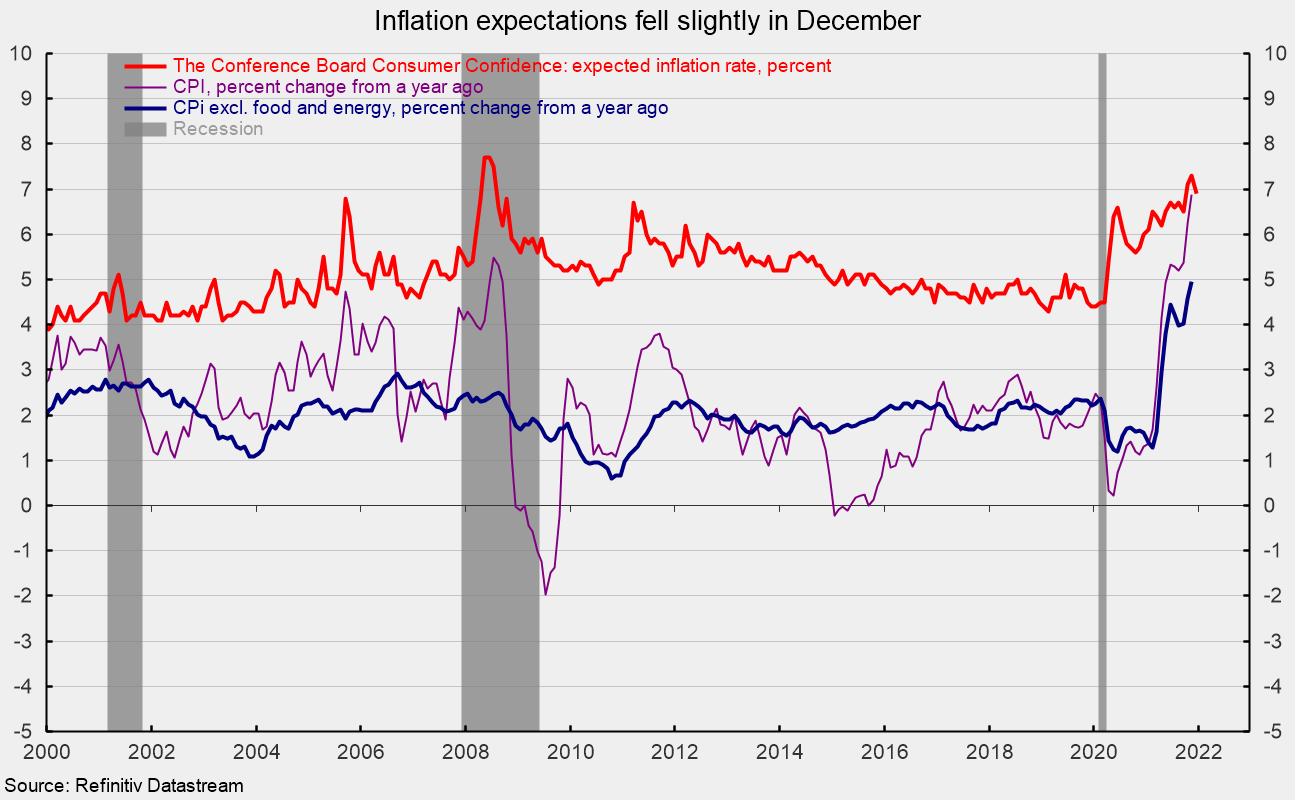

Inflation expectations fell to 6.9 percent in December, down from 7.3 in November; expectations were 4.4 percent in January 2020 (see second chart). Historically, consumers’ inflation expectations have been well above actual inflation measures (see second chart).

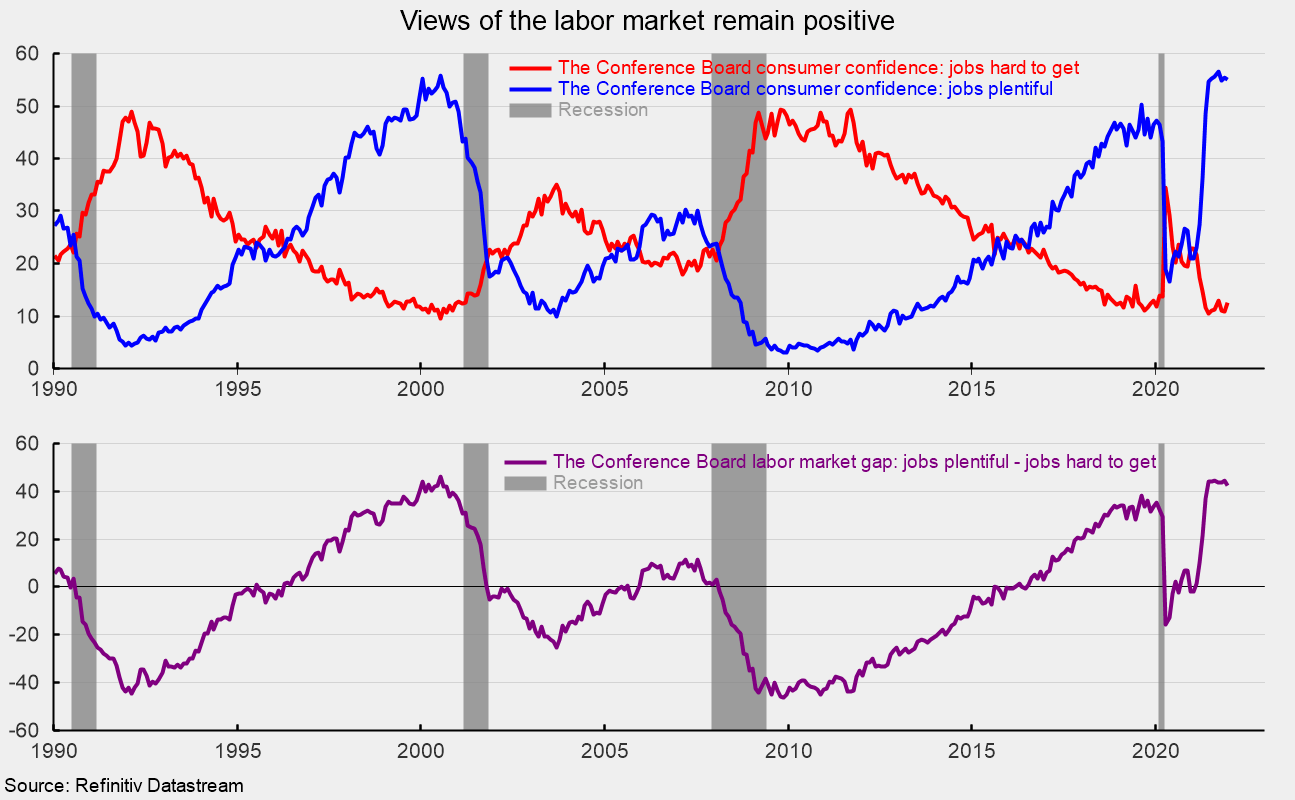

While inflation views have worsened significantly since the start of the pandemic, views of the labor market remain a strong support for overall consumer confidence. Current views for the labor market saw the jobs hard to get index rise 1.7 points to 12.5 (see top of third chart) while the jobs plentiful index fell 0.4 points to 55.1 (see top of third chart) resulting in a 2.1-point decline in the net to a still-strong 42.6 (see bottom of the third chart).

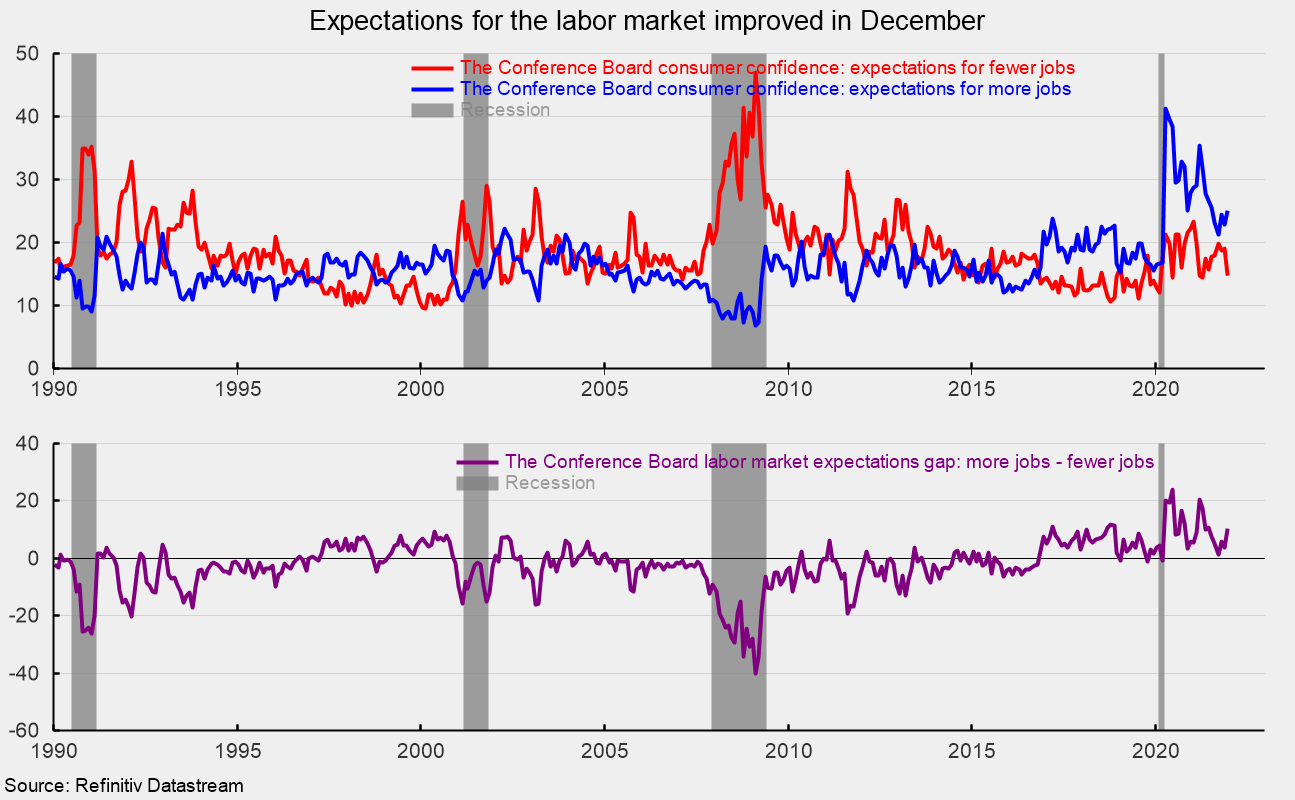

The outlook for the jobs market improved sharply in December as the expectations for more jobs index rose 2.3 points to 25.1 (see top of fourth chart) while the expectations for fewer jobs index sank by 4.2 points to 14.8 (see top of fourth chart) putting the net up 6.5 points to 10.3 (see bottom of fourth chart).

The outlook for the economy is for continued expansion. However, ongoing shortages of materials, labor difficulties, and logistical problems are sustaining upward pressure on prices and weighing on consumers’ attitudes. A strong labor market offsets the negative views of inflation, resulting in generally moderate consumer confidence. Continued waves of new Covid cases remains a threat to consumer confidence and the economy.

0 Comments