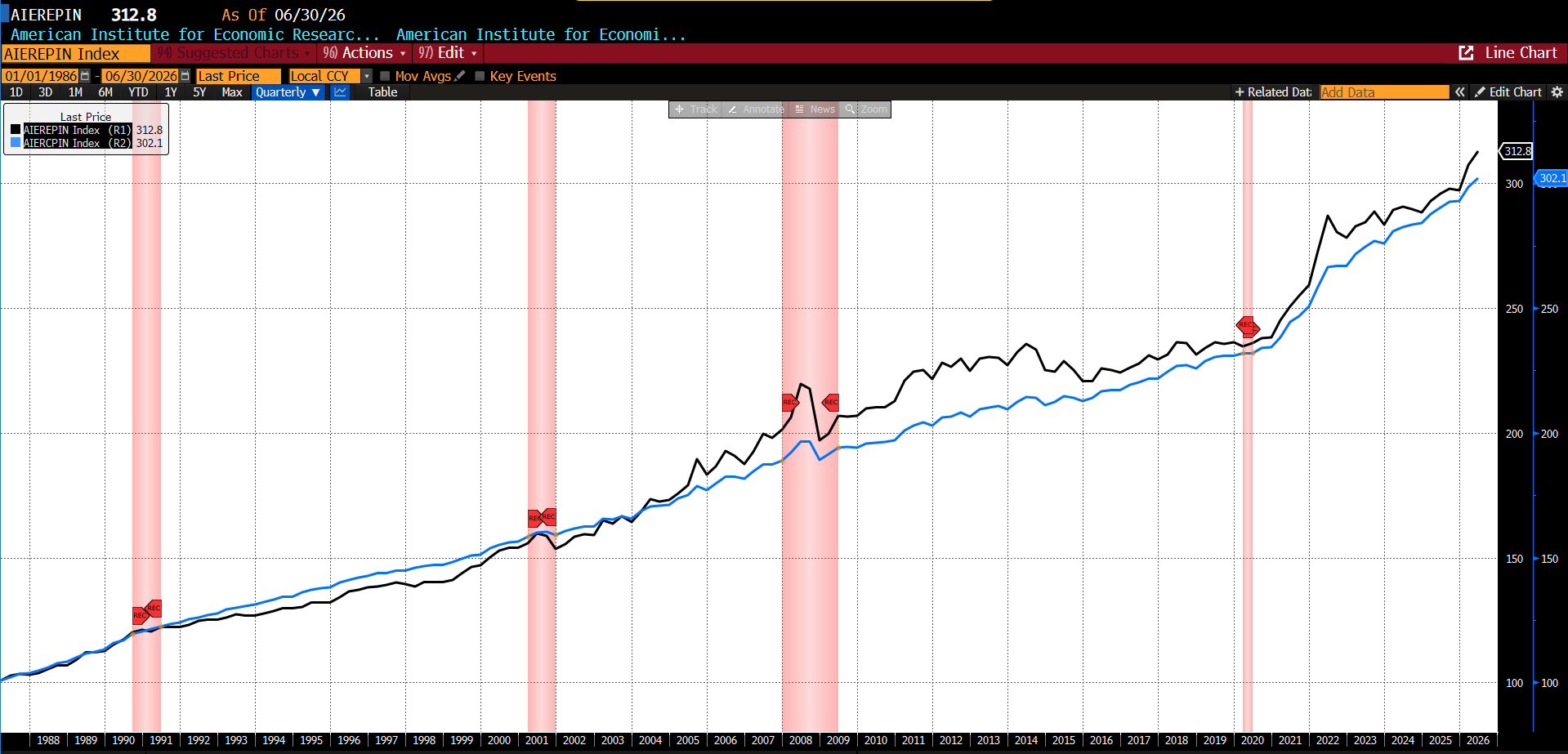

The AIER Everyday Price Index (EPI) fell to 312.8 in June 2026, down from 316.0 in May. The 1.02 percent monthly decline reversed part of May’s sharp energy-driven increase and brought the index down by roughly 3.2 points. Fifteen EPI categories rose, eight declined, and no indicator was unchanged, but the sizable drop in motor fuel more than offset price increases elsewhere.

The largest monthly decline came from motor fuel, which fell 9.6 percent in June. Other notable declines included movie and theater admissions, tobacco and smoking products, and purchase, subscription, and video rentals. The largest increases came from gardening and lawncare services, intracity transportation, personal care services, and fuels and utilities. Food away from home and food at home also rose, but not by enough to counteract the decline in gasoline-related costs.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

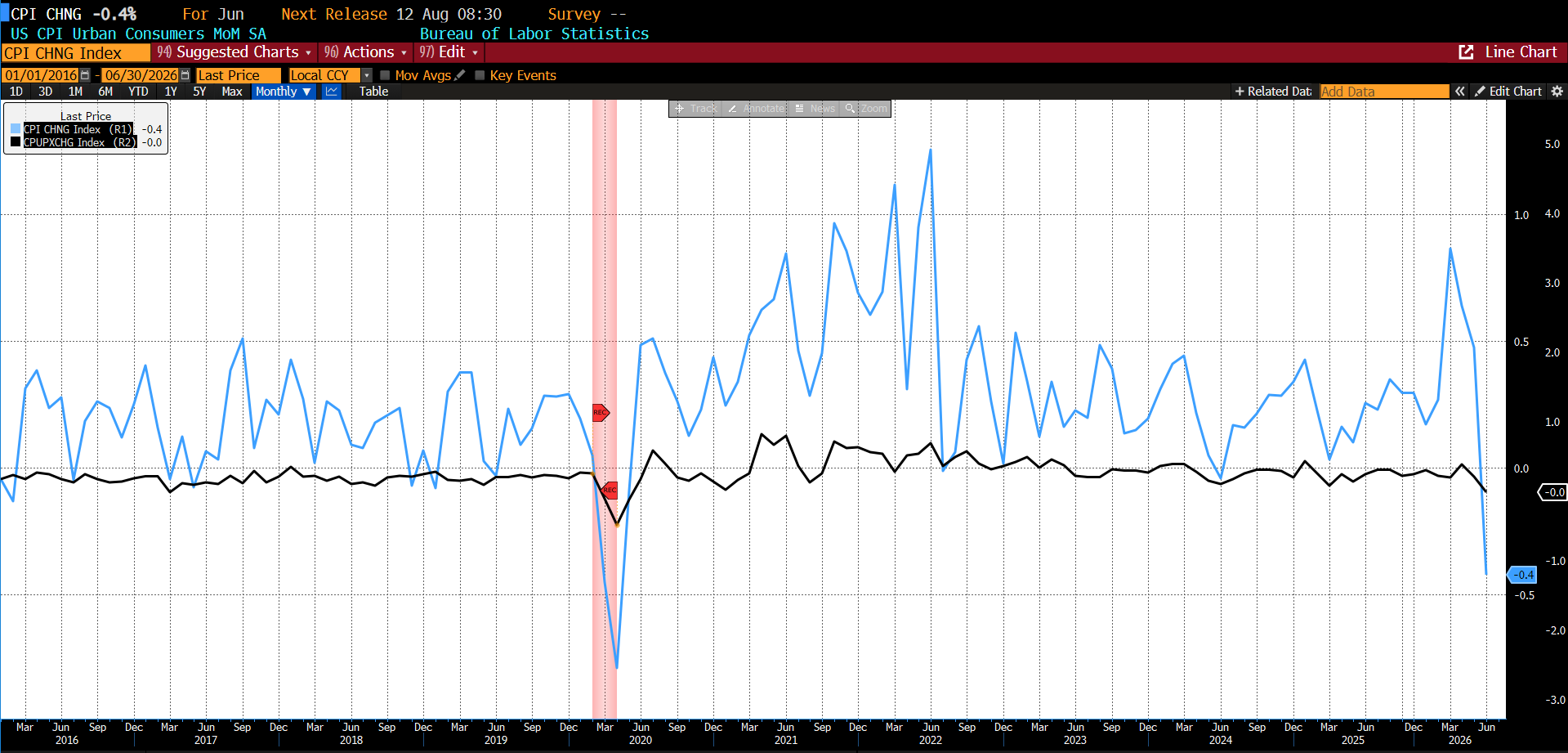

Also on July 14, 2026, the US Bureau of Labor Statistics (BLS) released the June 2026 Consumer Price Index (CPI) data. Headline CPI fell 0.4 percent on a seasonally adjusted basis in June after rising 0.5 percent in May; this was the largest one-month decline since April 2020. Core CPI, which excludes food and energy, was unchanged in the month after increasing 0.2 percent in May.

June 2026 US CPI headline and core month-over-month (2016 – present)

Consumer prices in June were driven overwhelmingly by a reversal in energy costs. The energy index fell 5.7 percent after rising 3.9 percent in May, 3.8 percent in April, and 10.9 percent in March. Gasoline prices declined 9.7 percent on the month, both seasonally adjusted and before seasonal adjustment, making energy the largest contributor to the decline in the all-items CPI. Electricity fell 1.0 percent, while utility gas service rose 0.5 percent.

Food prices continued to rise, though moderately. The food index increased 0.2 percent in June, as did food at home and food away from home. Within groceries, meats, poultry, fish, and eggs rose 0.6 percent, with eggs up 4.3 percent. Dairy and related products increased 1.2 percent, cereals and bakery products rose 0.3 percent, and other food at home increased 0.5 percent. Offsetting those gains, nonalcoholic beverages fell 1.5 percent, helped by a 2.0 percent decline in coffee prices, while fruits and vegetables slipped 0.2 percent.

Core inflation softened notably. The index for all items less food and energy was unchanged in June, with several categories declining outright. Motor vehicle insurance fell 2.0 percent, communications declined 1.5 percent, apparel fell 0.6 percent, medical care slipped 0.1 percent, and used cars and trucks declined 0.2 percent. Shelter rose only 0.1 percent, its smallest monthly increase since January 2021. Rent of primary residence rose 0.1 percent, owners’ equivalent rent increased 0.2 percent, and lodging away from home fell 2.3 percent.

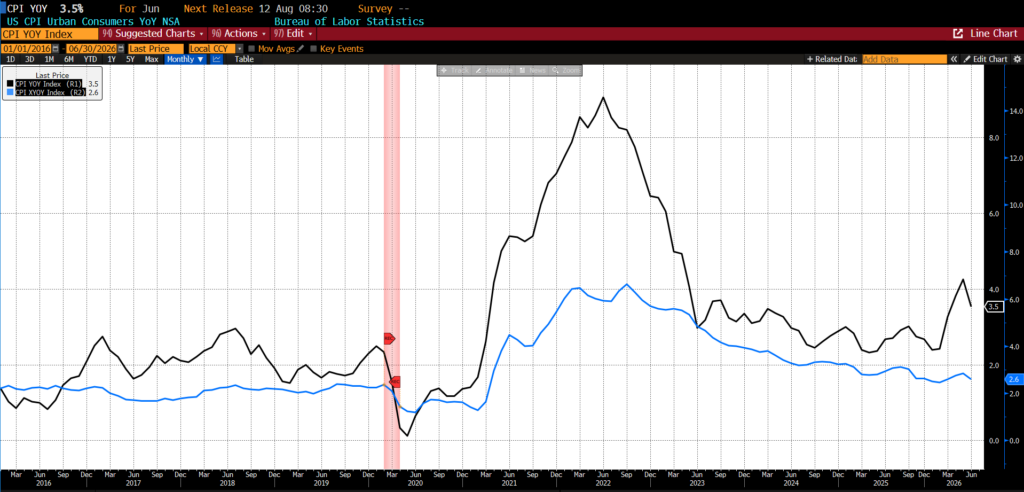

Over the twelve months ending in June 2026, headline CPI rose 3.5 percent, down from 4.2 percent in May. Core CPI increased 2.6 percent over the year, following a 2.9 percent annual increase in May.

June 2026 US CPI headline and core year-over-year (2016 – present)

From June 2025 to June 2026, food inflation remained moderate but persistent. Food at home rose 2.7 percent over the year, while food away from home increased 3.4 percent. Fruits and vegetables rose 5.3 percent, other food at home increased 2.4 percent, meats, poultry, fish, and eggs rose 2.6 percent, nonalcoholic beverages advanced 2.9 percent, and cereals and bakery products increased 2.4 percent. Dairy prices were nearly flat, rising only 0.4 percent over the year.

Energy remained the dominant annual inflation story despite June’s monthly pullback. The energy index increased 15.7 percent over the twelve months ending in June, with gasoline prices still up 26.7 percent from a year earlier. Electricity rose 4.0 percent and utility gas service increased 3.0 percent over the same period. Thus, while June brought meaningful short-term relief at the pump, energy costs remained substantially higher than a year earlier.

Core inflation was less dramatic but still broad enough to matter. Prices excluding food and energy rose 2.6 percent over the year. Shelter increased 3.3 percent, continuing to anchor underlying inflation, while medical care rose 2.0 percent, recreation increased 2.8 percent, and household furnishings and operations advanced 2.5 percent. Airline fares remained one of the most striking annual increases, rising 26.5 percent from June 2025, even as they eased modestly on the month.

The June CPI report provided the clearest evidence yet that the spring 2026 energy shock is beginning to reverse. After gasoline and other fuel costs drove inflation sharply higher in March through May, June brought falling gasoline prices, a lower headline CPI reading, and a decline in AIER’s EPI. For consumers, this was particularly significant because gasoline is among the most visible and psychologically influential prices they face. Even so, affordability remains strained as shelter, dining out, and many service-sector prices continue to rise, leaving June looking more like a pause in an energy-driven inflation surge than the end of the inflation problem.

The report also reshaped the Federal Reserve’s near-term outlook. Chair Kevin Warsh has emphasized that restoring price stability remains the Fed’s overriding priority, but the softer June inflation data reduce the urgency for another rate hike while allowing policymakers to maintain a hawkish tone. Markets responded by substantially lowering the probability of a near-term increase in interest rates, suggesting the Fed can afford to wait for additional evidence from future inflation reports, labor-market conditions, and energy prices before deciding whether further tightening is warranted.

That patience, however, comes with risks. June’s improvement depended heavily on lower gasoline prices, leaving inflation vulnerable to renewed geopolitical disruptions, higher oil prices, tariffs, or continued AI-related investment pressures that could reignite cost increases. While the Fed cannot produce more oil or resolve supply shocks, it must remain alert to the possibility that temporary increases in energy costs become embedded in inflation expectations, wage demands, and business pricing decisions. The result is a delicate balancing act: avoiding an unnecessary policy response to what may prove to be a temporary supply shock while ensuring that inflation does not become entrenched once again.

0 Comments