The Federal Reserve’s recent decision to cut the federal funds rate by 50 basis points to a range of 4.75 percent to 5 percent, despite inflation still exceeding its 2 percent target, bears alarming similarities to the monetary policy missteps of the late 1970s. Back then, under pressure to stimulate economic activity, the Fed loosened monetary policy too soon.

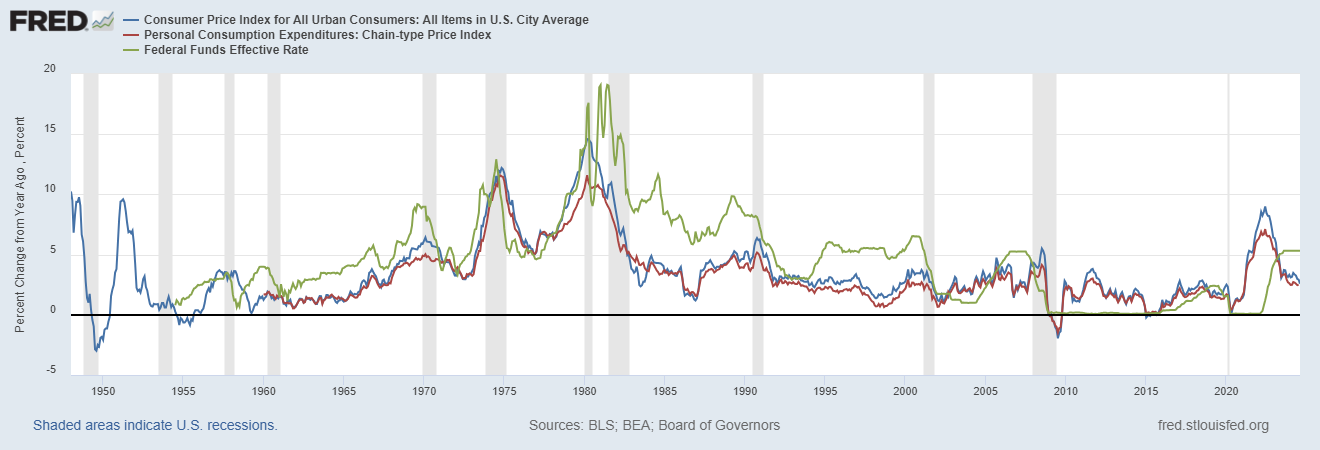

What was the result? Inflation soared as high as, if not higher, depending on the inflation measure. This culminated in Fed Chairman Paul Volcker reining in the money supply, which drove interest rates even higher. The result was necessary though painful double-dip recession before inflation persisted at a lower rate and the economy expanded during what’s been called the “Great Moderation.”

The recent Fed decision comes when inflation, though moderating, remains elevated. According to the latest Consumer Price Index (CPI) data, inflation increased by 2.5 percent year-over-year in August, with core inflation (less food and energy) rising by 3.2 percent. The Personal Consumption Expenditures (PCE) price index, the preferred core inflation measure for the Fed, showed a 2.6 percent year-over-year increase in July, further confirming that inflation is well above the 2-percent average inflation rate target (FAIT).

The risk is clear: repeating the premature rate cuts of the 1970s could ignite inflation once more, forcing even harsher corrective measures later.

The Fed’s Balance Sheet Problem

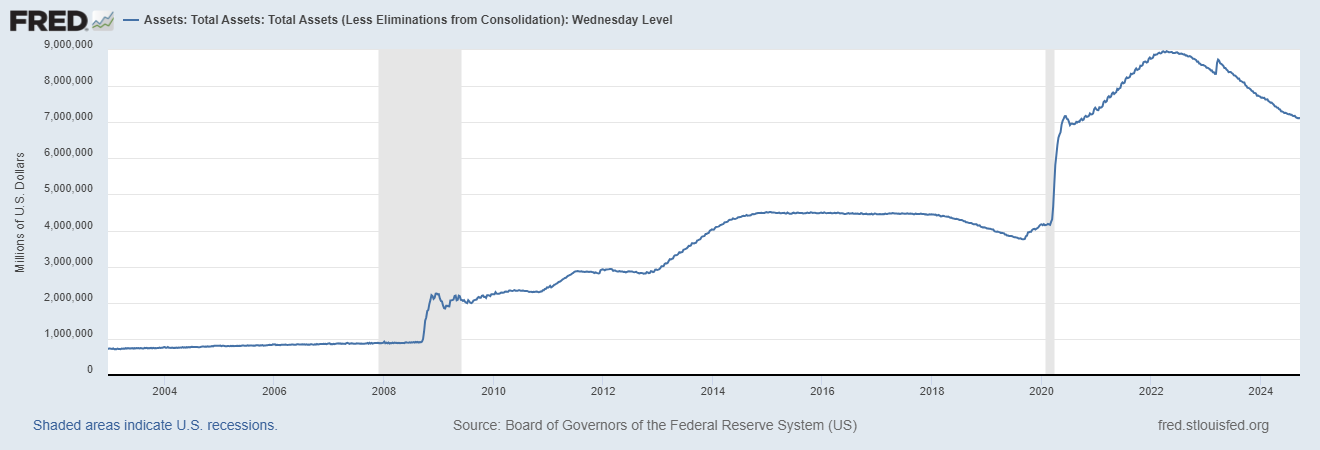

The Federal Reserve’s balance sheet expanded dramatically during the COVID-19 pandemic, nearly doubling from $4 trillion in February 2020 to nearly $9 trillion in April 2022. While the Fed has made some progress in reducing its balance sheet, which now stands at $7.1 trillion, this figure remains 75 percent higher than its pre-pandemic level, with potentially risky assets. This massive increase in the money supply has distorted the economy, contributing to inflationary pressures by artificially boosting demand as supply hasn’t kept up.

Rather than relying on interest rate cuts, the Fed should be focused on aggressively reducing its balance sheet. Milton Friedman’s insights remain as relevant today as ever: inflation is “always and everywhere a monetary phenomenon.” The rapid expansion of the Fed’s balance sheet and the excessive money printing during the pandemic era are key contributors to the inflation we are battling now. Shrinking the balance sheet would help reduce the excess liquidity in the system, curbing inflation more effectively than rate cuts alone.

Distortive Power of Government Spending and Policy

While monetary policy is one part of the equation, we cannot overlook the role of fiscal policy in the current inflationary environment. Government spending has exploded since 2020 during the pandemic lockdowns, with the gross national debt soaring by nearly $13 trillion since 2019 to $35.3 trillion. The House of Representatives, rather than addressing this spending crisis, is set to pass another spending bill ahead of the September 30 deadline. As currently designed, this bill includes little in the way of meaningful spending restraint. Kicking the can down the road without addressing the structural imbalance in government finances only weakens the economy.

When the government spends recklessly by redistributing productive private resources to fund politically determined provisions, this contracts the potential supply of goods and services. And with the Fed printing so much money over the last few years, we have a clear explanation for the persistent general price inflation that reached a high of 9 percent in June 2022. But the inflationary pressures remain in the economy. This creates a vicious cycle, where excessive government borrowing leads to higher interest payments, necessitating further borrowing and money printing by the Fed to keep interest rates near its target. The only way to break this cycle is through fiscal discipline — capping government spending, reducing the deficit, and removing unnecessary programs — and more economic growth.

The government’s heavy-handed interventions in the form of taxes, regulations, and excessive spending distort market signals, stifle entrepreneurship, and create inefficiencies. These interventions raise business costs, leading to higher consumer prices and reduced economic growth. Rather than focusing on rate cuts and temporary relief, policymakers should aim for long-term solutions addressing inflation’s root cause: excessive money printing.

The Fed’s Mixed Messages

The Federal Open Market Committee’s (FOMC) latest statement signals an optimistic view that inflation is making “further progress” toward the 2 percent target. The Committee also highlights that it has “gained greater confidence that inflation is moving sustainably” toward its goal. However, this confidence is misplaced, given the persistent inflationary pressures evident in the data. The energy index has declined 4 percent over the past 12 months, but core inflation remains stubbornly high, and key services sectors continue to experience rising prices.

Cutting rates under these conditions risks reigniting inflation, just as the Fed’s premature monetary policy, including rate cuts, in the late 1970s exacerbated inflation and led to economic instability. The FOMC’s decision to reduce the target range for the federal funds rate while signaling its commitment to further rate cuts, if “appropriate,” creates uncertainty in the markets. This mixed messaging signals that the Fed is willing to sacrifice long-term price stability for short-term gains, which could lead to more aggressive corrective actions. Given the double-dip recession in the early 1980s, there is reason for concern.

The Path Forward: Fiscal and Monetary Solutions

The Fed’s dual mandate is to ensure price stability and maximum employment. With inflation still above target, its focus should be on controlling inflation–its balance sheet and inflation are the only two things it can control. This highlights the need to make it a single mandate to ensure price stability rather than trying to stimulate economic growth. History teaches us that premature rate cuts — like those in the 1970s — lead to higher inflation, more aggressive rate hikes, and economic contraction.

A more prudent approach would involve reducing the Fed’s balance sheet more aggressively, which would help soak up the excess liquidity, fueling inflationary pressures. Moreover, Congress must confront the spending crisis head-on. A balanced approach to fiscal policy, with spending limits tied to a maximum rate of population growth and inflation, would help stabilize government finances and reduce the deficit. Even better is Sen. Rand Paul’s Six Penny Plan, a “federal budget resolution that will balance on-budget outlays and revenues within five years by cutting six pennies off every dollar projected to be spent in the next five fiscal years.” Without these structural reforms, inflation will continue to threaten the purchasing power of Americans.

Furthermore, the government should remove barriers to productivity by cutting excessive regulations and taxes that stifle growth. Allowing the free market to operate efficiently without the distortive effects of heavy-handed government policies will promote sustainable, long-term growth.

Conclusion: A Critical Moment for the Economy

The Federal Reserve and Congress are at a critical juncture. The Fed’s decision to cut rates prematurely risks repeating the costly mistakes of the 1970s, where loose monetary policy fueled inflation, leading to severe economic instability. Simultaneously, Congress’s reluctance to tackle deficit spending driving the ballooning national debt only exacerbates the underlying issues plaguing the economy.

Now is not the time for short-term fixes. The Fed should focus on reducing its balance sheet and controlling inflation, while Congress must enact serious spending reforms to prevent further economic deterioration. If we fail to act now, we risk plunging into an inflationary spiral reminiscent of the 1970s — a government-induced failure the American economy cannot afford.

0 Comments