The disinflation process has not been as consistent as one may have hoped, new data from the Bureau of Economic Analysis show. The Personal Consumption Expenditures Price Index (PCEPI), which is the Federal Reserve’s preferred measure of inflation, grew at a continuously compounding annual rate of 3.4 percent over the twelve-month period ending in September 2023—down from 6.4 percent over the twelve-month period ending in September 2022. That’s the good news. But there’s also bad news.

Although inflation has declined over the last year, it has rebounded in recent months. Over the three-month period ending September 2023, prices grew at an annualized rate of 3.7 percent, compared with 2.3 percent over the three-month period ending June 2023. The uptick is especially pronounced in the last two months. In August 2023, reduced energy supplies caused prices to grow at an annualized rate of 4.4 percent, up from 2.5 percent in the prior month. In September, prices grew at an annualized rate of 4.3 percent.

There are two distinct reasons to be concerned about the recent rise in inflation. First, one might worry about an inflation resurgence, with prices growing as fast as they did in late 2021 and 2022—or, at least faster than they were growing just a few months ago.

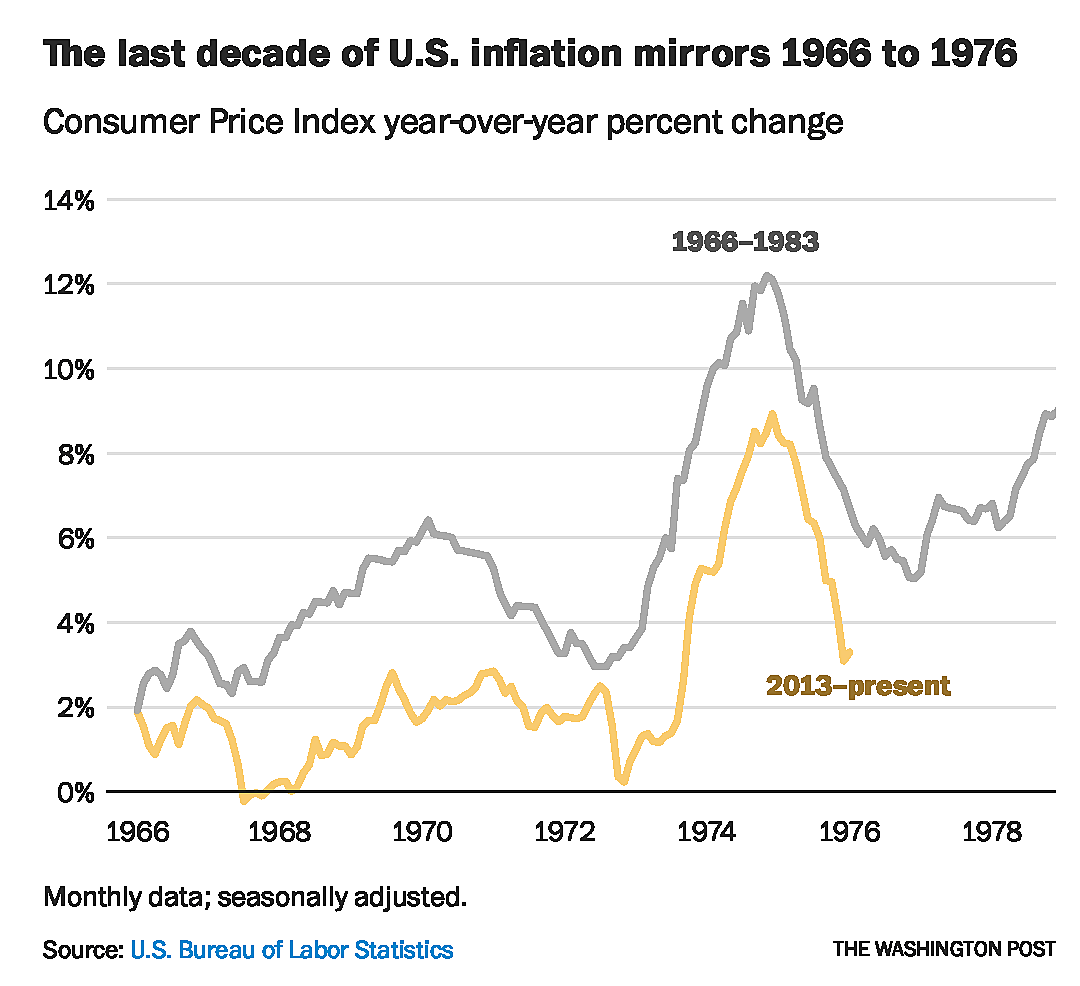

Some point to the two waves of inflation experienced in the 1970s. “It is sobering to recall,” former Treasury Secretary Lawrence Summers wrote in August, “that the shape of the past decade’s inflation curve almost perfectly shadows its path from 1966 to 1976 before it accelerated in the late 1970s.”

One should be very skeptical when presented with a supposed pattern in macroeconomic data. There is no reason to think prices will inevitably evolve today as they did then. At most, the prior episode indicates that it can happen. If one believes that it will happen, one should identify the causal factors.

Perhaps the best argument that inflation will rise again relates to fiscal policy. Short-term interest rates are higher than they have been at any point in the last twenty years. Consequently, the federal government’s interest expense has exploded. To deal with the additional expense, the government must (1) increase revenues, (2) reduce expenditures, or (3) issue more debt. There seems to be little appetite in DC for raising taxes or cutting spending. The most likely outcome is that the government will issue more debt.

Additional government borrowing would put upward pressure on the natural rate of interest. To prevent inflation, the Fed would need to offset the fiscal expansion by raising its interest rate target. Otherwise, the spread between the natural rate and the Fed’s target will shrink, passively loosening monetary policy. Hence, inflation could rise again if the Fed fails to offset expansionary fiscal policy.

Another reason to be concerned about the recent rise in inflation is that it increases the odds that the Fed will overtighten.

The (nominal) federal funds rate target range is currently set at 5.25 to 5.5 percent. With core PCEPI inflation at 3.6 percent in September, the real federal funds rate target is probably somewhere between 1.65 and 1.9 percent. For comparison, the New York Fed currently estimates the natural rate of interest at 0.57 to 1.14 percent. Monetary policy appears to be sufficiently tight.

Nonetheless, at the September meeting of the Federal Open Market Committee, twelve members projected an additional rate hike in 2023. If anything, the inflation data released in September and October makes additional rate hikes more likely.

The Fed should keep monetary policy tight as inflation returns to its 2-percent target. But if it tightens too much, it will push the economy into an unnecessary and painful recession.

As I have written before, it is difficult to determine what the Fed should do when it hasn’t done what it should have done. It would have been better had it avoided this situation altogether. Obviously, it is too late for that now. We are where we are. One can only hope that the Fed will navigate this narrow pass safely this time—and steer clear of such dangers in the future.

0 Comments