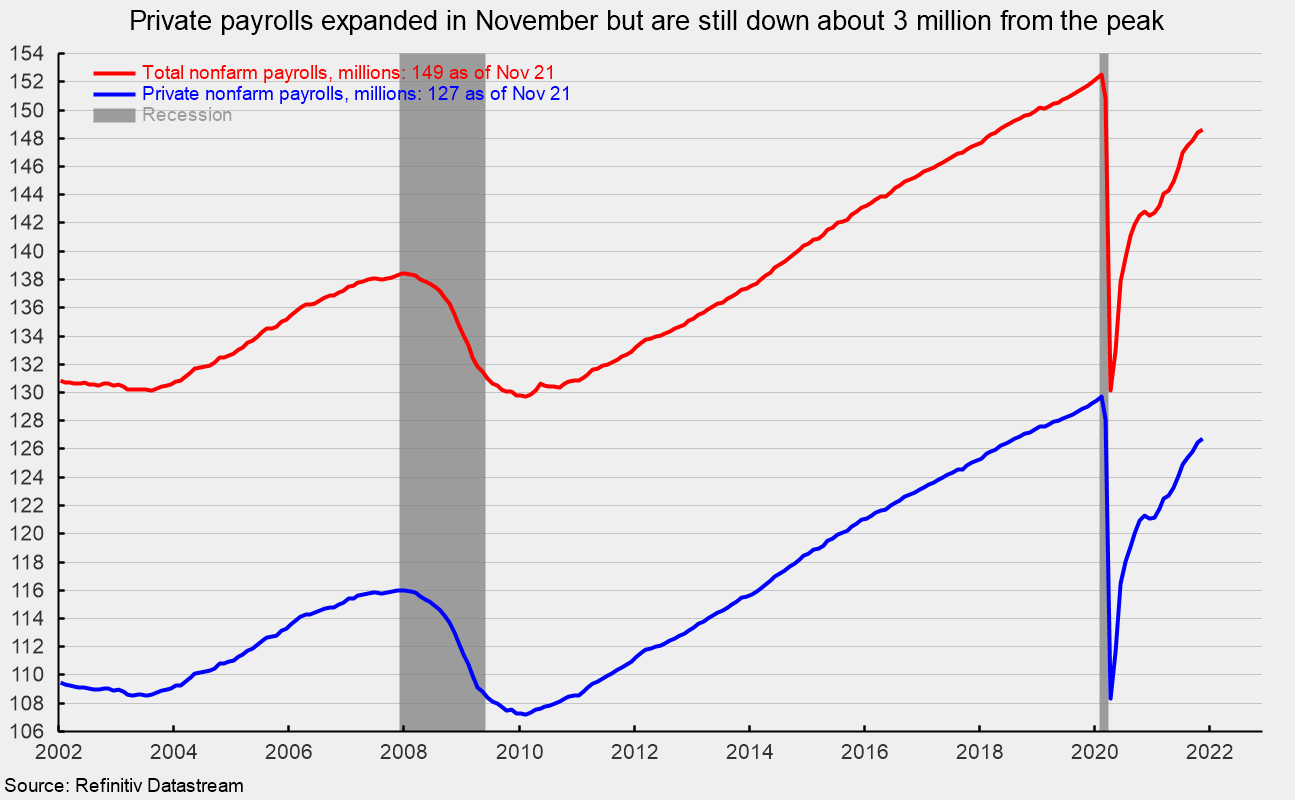

U.S. nonfarm payrolls added 210,000 jobs in November, a disappointing result. The gain follows upwardly revised additions of 546,000 in October and 379,000 in September. The November increase is the 11th in a row and 18th in the last 19 months, bringing the 11-month rise to 6.108 million and the 19-month post-plunge recovery to 18.450 million. This is still below the 22.362 million combined loss from March and April of 2020, leaving nonfarm payrolls 3.912 million below the February 2020 peak (see first chart).

Private payrolls posted a 235,000 gain in November after a 628,000 increase in October and 424,000 addition in September. Both months were revised up from their original estimates. The November rise in private payrolls is also the 11th in a row and 18th in the last 19 months. The November addition brings the 11-month gain to 5.664 million and the 19-month recovery to 18.376 million versus a combined loss of 21.353 million in March and April of 2020, leaving private payrolls 2.977 million or about 2.3 percent, below the February 2020 peak (see first chart).

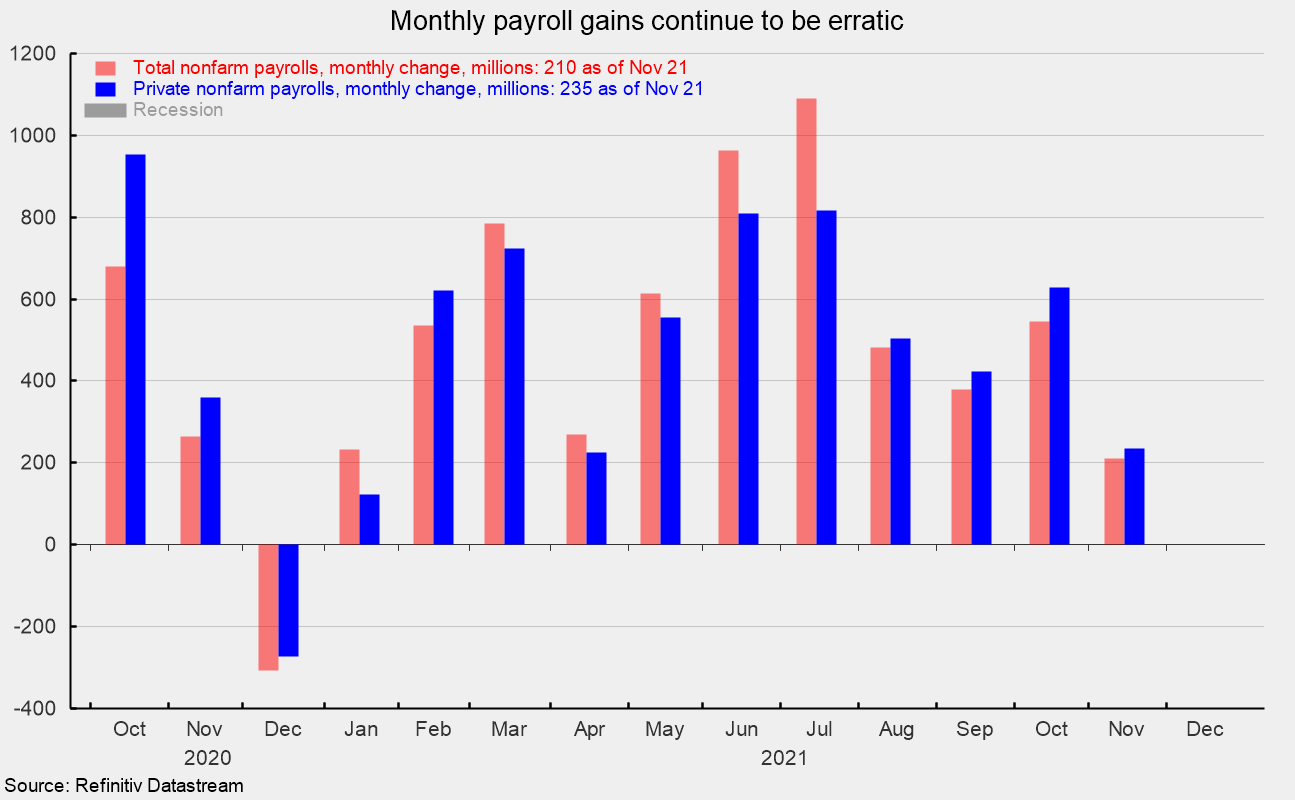

The recovery in payroll employment continues to be erratic, with large additions in some months but small increases in other months (and a loss in December 2020; see second chart). The 235,000 increase to private payrolls in November was about half (52 percent) of the 449,000 monthly average increase over the last 12 months. Resurgent waves of new Covid cases and deviations from typical hiring patterns in some industries that throw off seasonal adjustment are both likely contributors to the volatility.

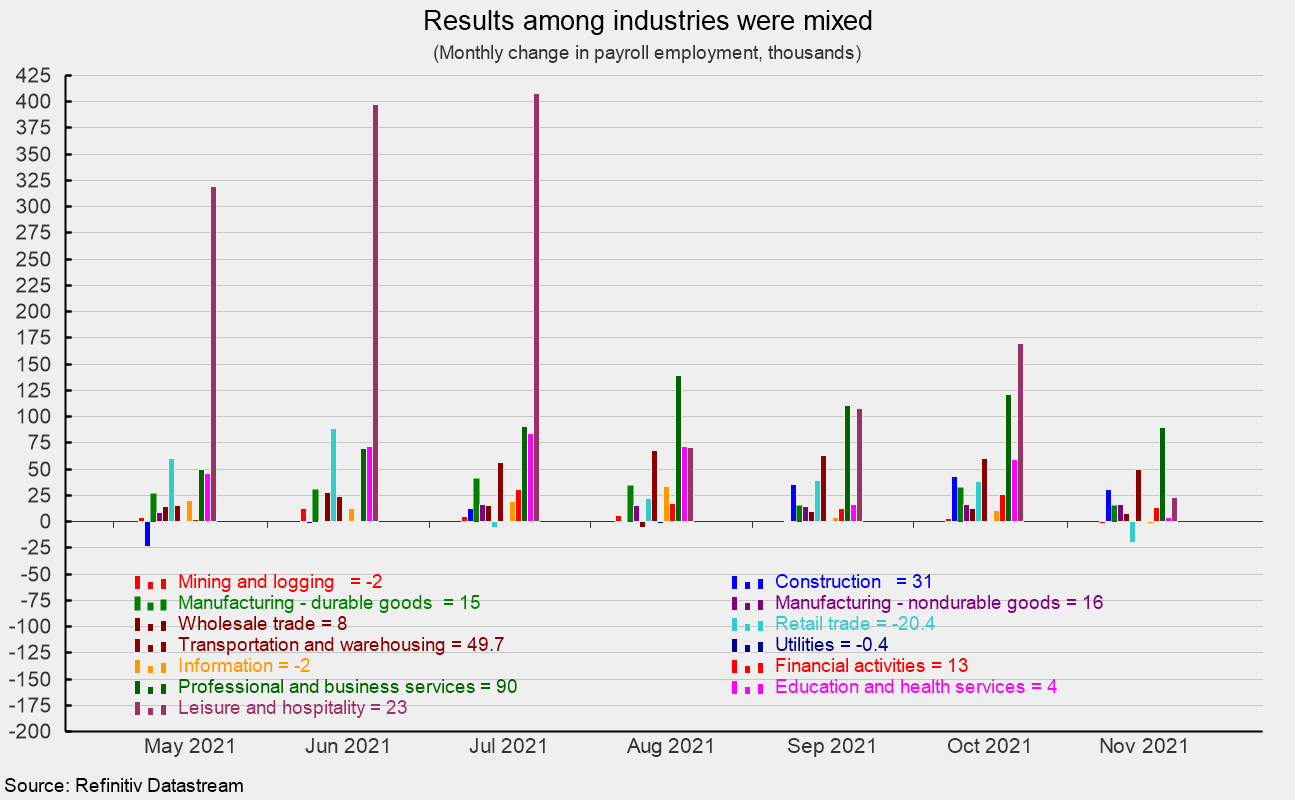

While the pace of gain has varied over the last 12 months, gains have been generally broad-based, though weakness in November was widespread (see third chart). Within the 235,000 gain in private payrolls, private services added just 175,000 versus a 12-month average of 401,000 while goods-producing industries added 60,000 versus a 12-month average of 48,000.

Within private service-producing industries, business and professional services added 90,000 (versus a 12-month average of 84,000) in November, transportation and warehousing gained 49,700 (versus 27,000), leisure and hospitality added 23,000 (versus 162,000) for the month, and financial activities gained 13,000 (versus 12,000). Retail employment fell by 20,400 versus an average monthly gain of 25,000 (see third chart).

Within the 60,000 gain in goods-producing industries, construction added 31,000, while durable-goods manufacturing increased by 15,000, nondurable-goods manufacturing added 16,000, but mining and logging industries decreased by 2,000 (see third chart).

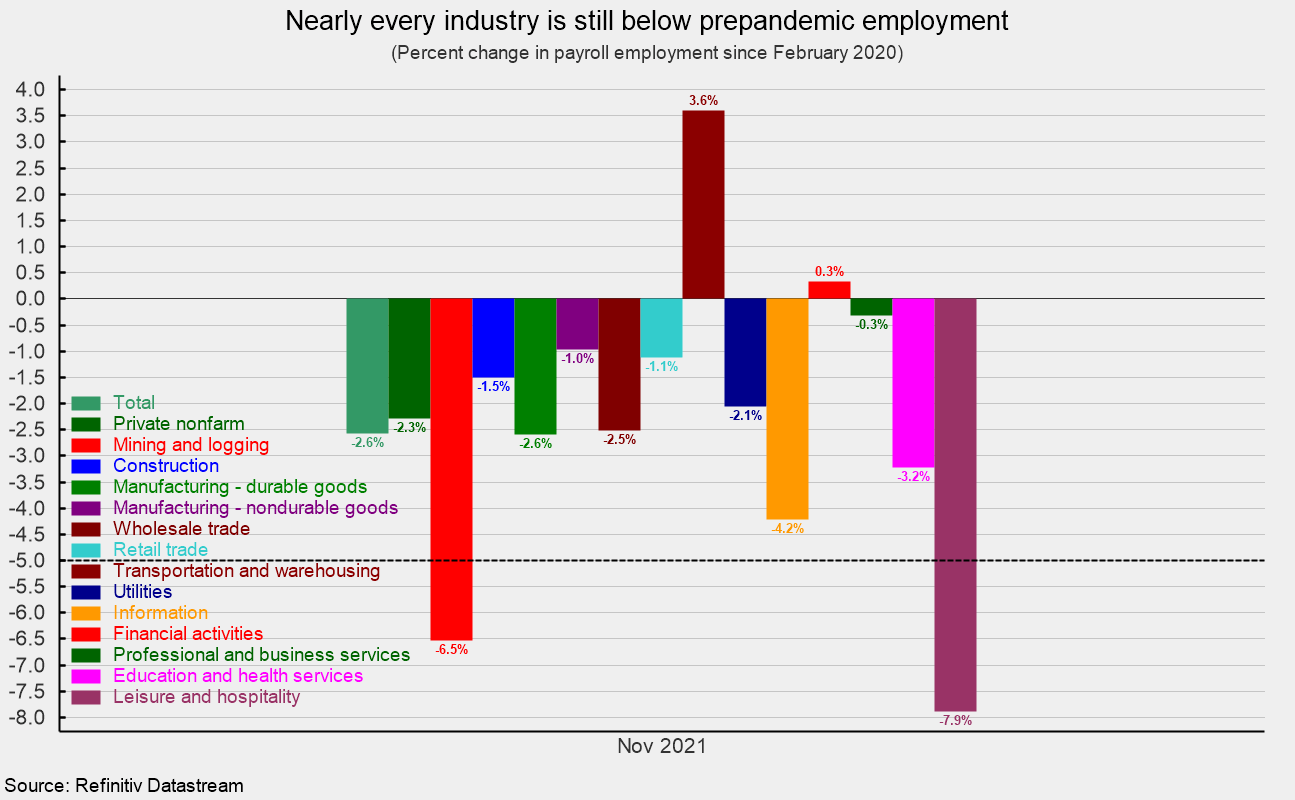

After 19 months of recovery, only two of the major private industry groups have more employees than before the government lockdowns – transportation and warehousing is 3.6 percent above the February 2020 level and financial activities is 0.3 percent above. Two industries – Leisure and hospitality (-7.9 percent) and mining and natural resources (-6.5 percent) – are still down more than five percent (see fourth chart).

Average hourly earnings rose 0.3 percent in November, putting the 12-month gain at 4.8 percent. The average hourly earnings data should be interpreted carefully, as the concentration of job losses and recovery for lower-paying jobs during the pandemic distorts the aggregate number.

The average workweek rose 0.1 hour to 34.8 hours in November. Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls gained 0.7 percent in November. The index is up 9.5 percent from a year ago.

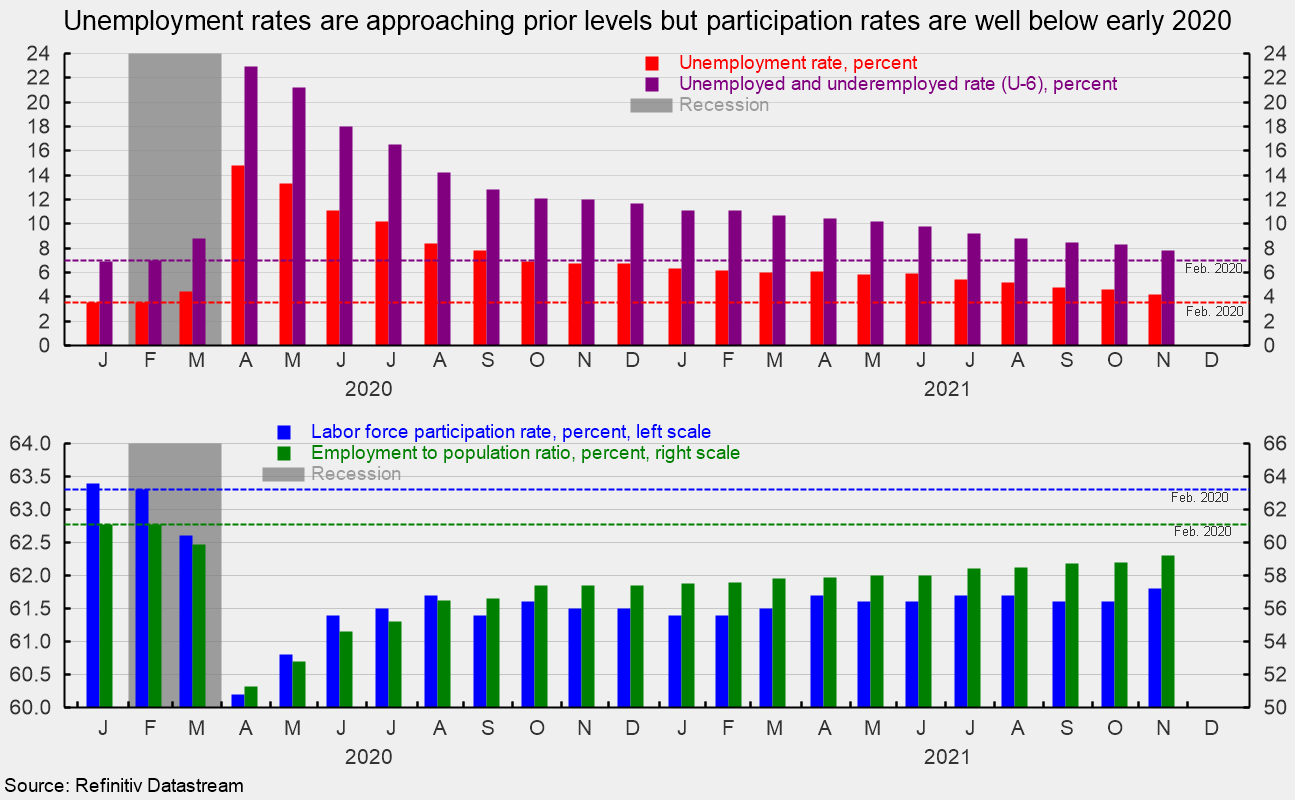

The total number of officially unemployed fell to 6.887 million, a drop of 542,000. The unemployment rate fell to 4.2 percent while the underemployed rate, referred to as the U-6 rate, fell to 7.8 percent in November. In February 2020, the unemployment rate was 3.5 percent while the underemployment rate was 7.0 percent (see top of fifth chart).

The participation rate increased by 0.2 percentage points in November, coming in at 61.8 percent versus a participation rate of 63.3 percent in February 2020. The employment-to-population ratio, one of AIER’s Roughly Coincident indicators, came in at 59.2 for November, up from 58.8 in October but still significantly below the 61.1 percent in February 2020 (see bottom of fifth chart).

The November jobs report shows total nonfarm payrolls posted a disappointing gain of 210,000 in November. Private payrolls were slightly better at 235,000 but both were significantly below their 12-month average gain and below expectations. It is likely that recurring waves of new Covid cases and a scarcity of potential workers are preventing a faster recovery in payroll employment.

Difficulty in hiring is likely to prolong the ongoing materials shortages, production constraints, and logistical and transportation bottlenecks that are sustaining significant upward pressure on prices. Overall, the outlook is for continued recovery; however, as waves of new Covid cases hamper efforts to hire and increase production, upward price pressures are likely to continue for a prolonged period.

0 Comments