Treasury Secretary Janet Yellen warns that the US may be unable to pay its bills as soon as December 15th unless Congress raises or suspends the federal debt limit. That limit was increased to $28.4 trillion on August 1 before being suspended the next day, then raised again to $28.88 trillion in October to stall through December 3. Secretary Yellen’s threat failed to intimidate Congress, which just passed a bipartisan $1 trillion infrastructure bill, or the House Democrats who added an underestimated $2 trillion Build Back Better bill. Yet Senate Republicans are expected to indulge in yet another futile game of bluff poker over the symbolic debt limit. They always fold in the end because Congress has no choice but to pay for obligations it has already incurred.

Congress first set a debt limit of $5 billion in April 1917 on borrowing for World War I, but later raised it to $43 billion by the time the war ended in 1918. It did not work then and has never worked since. If debt limits were at all effective, federal debt could not have soared to 125.5% of GDP in this year’s second quarter from 61.6% of GDP in the second quarter of 2007.

Republicans who hope to discourage runaway borrowing and spending do not have to keep relying on a failed 1917 law. They can replace it.

There is a much smarter way for Republicans to oppose endless budgetary excess –one that has a chance of making a lasting difference. Instead of trying to block appropriations already passed, the GOP can offer legislation that clearly covers all the bills the United States has incurred. But this bill would include a key condition: If the publicly held national debt exceeds a certain percentage of the current annual GDP (currently about 125%), the Federal Reserve would be restricted from holding more than a stated percent of that debt (currently about 25%). At that point, the Fed’s hoard of Treasury IOUs could not grow faster than the American economy that undergirds the debt and bankrolls the required interest payments.

The proposed “Debt Monetization Limit” would ensure that the Federal Reserve’s enormous mountain of Treasury IOUs could never again grow faster than GDP. The Treasury could still offer to sell all the bonds and bills needed to fund expenses that exceed revenues. But legislators could no longer count on the convenience of having a friendly central banker handy to mop up massive issues of Treasury securities if they proved difficult to peddle at home or abroad without offering a higher yield.

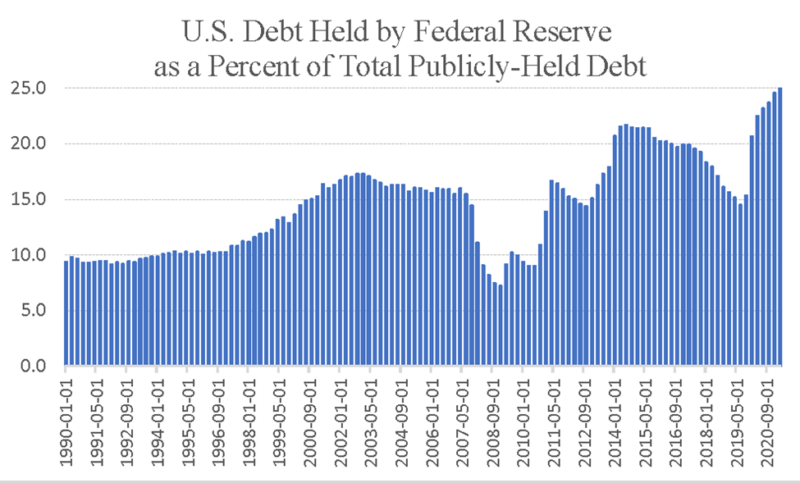

Ten years ago, many worried about China holding over $1 trillion in U.S. government debt, but that now looks like small change compared with the $5.64 trillion held by the Fed in the second quarter. Once called “the lender of last resort,” for a spendthrift Congress the Fed has become the lender of first resort.

The graph shows Federal debt held by Federal Reserve Banks as a rising percentage of all debt held by the public. The Great Recession was a brief anomaly, with the Fed reducing its holdings nearly 40% between the first quarter of 2007 and third quarter of 2008. That strangely timed quantitative tightening was followed by three waves of quantitative easing that can be seen in the graph starting in March 2009, November 2010, and September 2012. Most recently, Covid-19 and related lockdowns brought a deep two-month contraction which ended April 2020, according to the National Bureau of Economic Research. But the pandemic also brought a fourth tidal wave of quantitative easing – or what we used to call “monetizing the debt.”

The effects of the 2009-2014 quantitative easing experiments on interest rates or the economy remain unclear and questionable. During QE1 ($1.5 trillion) the 10-year Treasury yield rose from 2.97% on March 16 to 3.84% on March 31, 2010, then fell after QE1 ended. During QE2 ($827 billion) the 10-year yield fell from 2.67% on November 3, 2010 to 1.67% by June 29, 2012, but yields dipped even lower for months after it ended. Under QE3, yields rose from 1.86% at the start of 2013 to 3.04% by the end of the year, but then fell steadily to 2.34% by the end of the famous “taper” in October 2014 and continued falling after that.

The one certain effect of the Fed’s four bond-buying sprees (including 2020-22) is that they aided and abetted an increase in the publicly held national debt from 80.3% of GDP in the first quarter of 2009 to 125.5% in the first quarter of this year.

Once a central bank becomes habitually disposed to accommodate the government’s financial needs, there is little practical difference between the Treasury printing money and the Federal Reserve doing so. To answer a Frequently Asked Question, “Is the Federal Reserve printing money in order to buy Treasury securities?” the Federal Reserve Board’s website insists they merely print bank reserves, not money: “The increase in the Federal Reserve’s holdings of Treasury securities is matched by a corresponding increase in reserve balances held by the banking system. The banking system must hold the quantity of reserve balances that the Federal Reserve creates.”

The flip side of unrestrained Federal Reserve bond buying, in other words, is that bank reserves soared to $4.19 trillion in September – up from $46 billion in July 2008 when no interest was paid on reserves. Reserves used to be called “high-powered money” because when reserves were scarce, adding more reserves enabled banks to make many more loans, creating new money in the process by depositing borrowed sums into checking accounts. Until recently, such new deposits were limited by required reserves. But the superfluity of reserves removed that restraint as well as pressure to borrow reserves from the Fed’s discount window or the federal funds market. The main remaining restraint – since October 6, 2008 – is that the Fed could raise the interest rate it pays on reserves to a level high enough to keep banks content with leaving reserves idle rather than lending against them. In a grave error, the Fed did just that at the start of the 2008-2009 Great Recession.

Would limiting the Fed’s ability to influence interest rates through unlimited open-market purchases of Treasury notes and bills hinder its ability to conduct monetary policy? No – not after the explosion of bank reserves since 2009. Since the Fed began paying interest on trillions of dollars of bank reserves, changing that interest rate would have far more impact on bank lending than piling up even larger piles of superfluous reserves (though lowering that rate would now be foolhardy).

In any event, the GOP could enact a prudent forward-looking limit on the Fed’s ability to own government debt that is close enough to current practice to have little immediate effect on monetary or fiscal policy. In doing so, Republicans would achieve two important objectives. The first is political: to show their base that the party still has the will to fight for fiscal responsibility. The second is strategic: to make the issue of the Fed’s apparently limitless ability to expand the money supply a part of the political dialogue.

The Democrats may accept this GOP proposal. And if they do not, they will probably pass an old-fashioned debt limit bill in a big hurry through budget reconciliation. Following any other course would result in Democrats rather than Republicans facing the voters’ wrath for mismanaging the country’s finances.

0 Comments