Total housing starts fell to a 1.520 million annual rate in October from a 1.530 million pace in September, a 0.7 percent decrease. From a year ago, total starts are up just 0.4 percent. However, total housing permits rose in October, posting a 4.0 percent gain to 1.650 million in October from 1.586 million in September (see first chart). Total permits are up 3.4 percent from the October 2020 level.

Starts in the dominant single-family segment posted a rate of 1.039 million in October versus 1.081 million in September, a drop of 3.9 percent, and are down 10.6 percent from a year ago. However, single-family permits experienced a 2.7 percent rise to 1.069 million versus 1.041 million in September. Single-family starts have been trending lower from a peak around the start of the year but the recent stabilization for permits suggests that housing demand may be getting some renewed support (see first chart).

Starts of multifamily structures with five or more units increased 6.8 percent to 470,000 and are up a robust 39.5 percent over the past year while starts for the two- to four-family-unit segment were up 22.2 percent at an 11,000-unit pace. Combined, multifamily starts were 7.1 percent to 481,000 in October and show a gain of 36.6 percent from a year ago.

Multifamily permits for the 5-or-more group rose 6.5 percent to 528,000 while permits for the two-to-four-unit category jumped 8.2 percent to 53,000. Combined, multifamily permits were 581,000, up 6.6 percent for the month (see first chart) and 28.0 percent from a year ago.

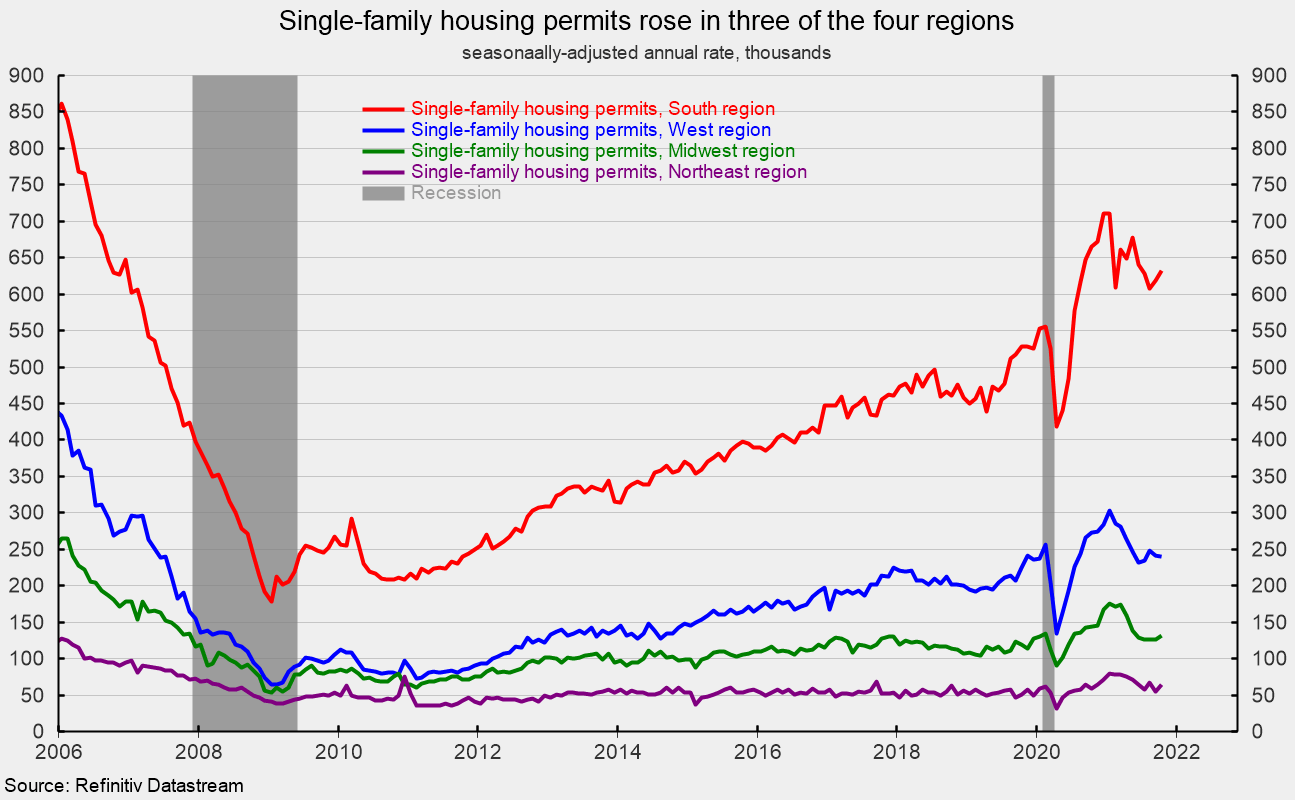

Regionally, single-family permits were up in three regions: the South (+2.3 percent), the Midwest (+4.8 percent), and the Northeast (+16.4 percent) had gains while the West (down 0.4 percent) fell (see second chart).

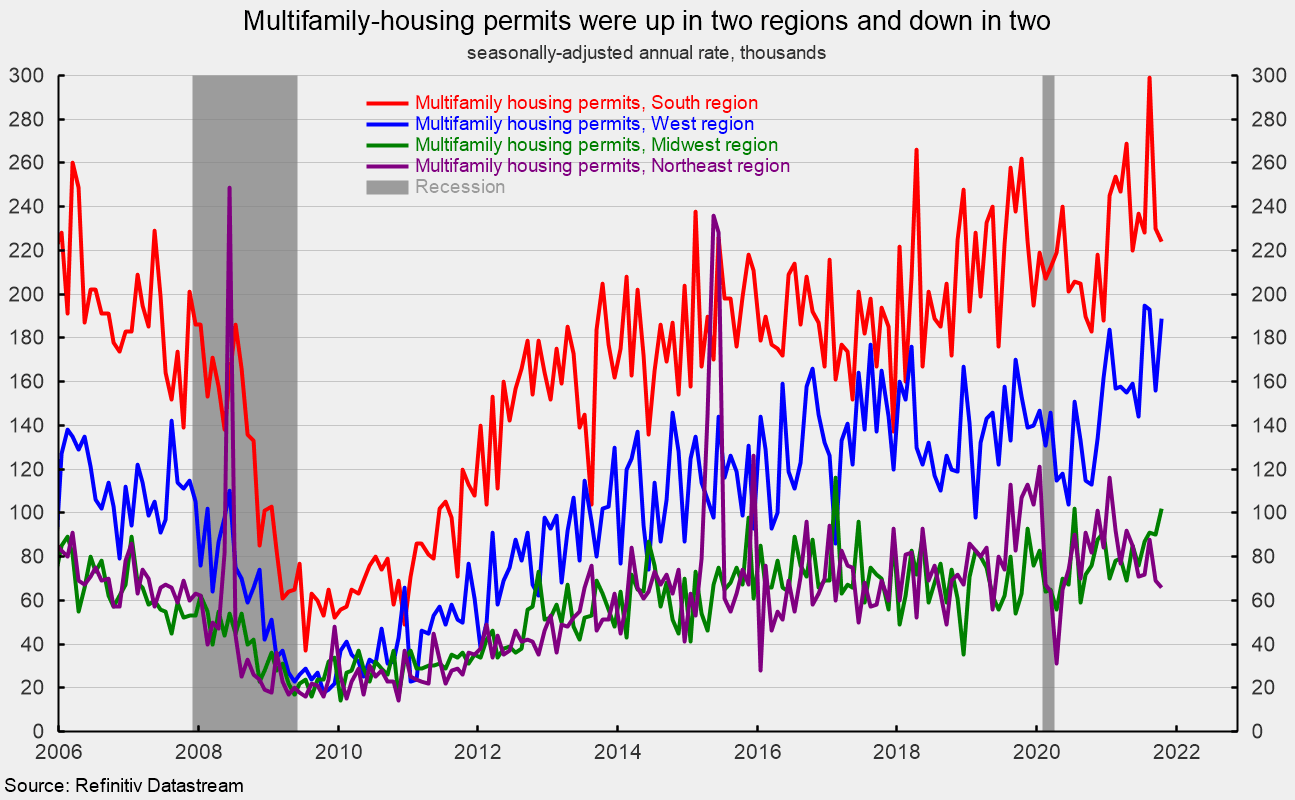

Multifamily permits had two regions with gains and two with declines in October. The South (off 2.6 percent) and the Northeast (down 4.3 percent) posted declines while the West (up 21.2 percent) and the Midwest (gaining 13.3 percent) posted increases (see third chart).

The surge in housing demand that sent lumber prices soaring to a peak of around $1,686 per 1,000 board feet had largely reversed course, hitting a low of around $450 in mid-September. However, since the low, lumber prices have started to rise again, hitting $667 in mid-November (see fourth chart). The rebound in lumber costs will pressure profits at builders and may lead to more price increases for new homes. Similarly, copper prices, another significant input in new home construction, remain elevated, coming in at $9,576 per metric ton in mid-November (see fourth chart).

Meanwhile, the National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, ticked up for a second month in a row in October, to 83 from 80 in September, but remains below the all-time peak of 90 in November 2020 (see fourth chart). Overall sentiment remains relatively high, but labor issues and supply chain disruptions continue to be significant problems.

Two of the three components of the Housing Market Index rose in October. The current single-family sales index rose to 89 from 86 in the prior month and the traffic of prospective buyers index was up three points to 68 but the expected single-family sales index remained unchanged at 84 in October.

The post-lockdown recovery in housing had been supported by a surge in demand as consumers sought less dense housing. However, since December, single-family activity has been trending lower, though the level of activity is still solid. It may be that some of the rush to less dense housing that drove the single-family surge in activity in the second half of 2020 is losing momentum as the economy opens, more people get vaccinated, and workers return to offices, though switching to permanent remote working arrangements by some employees may provide some extended support for housing.

0 Comments