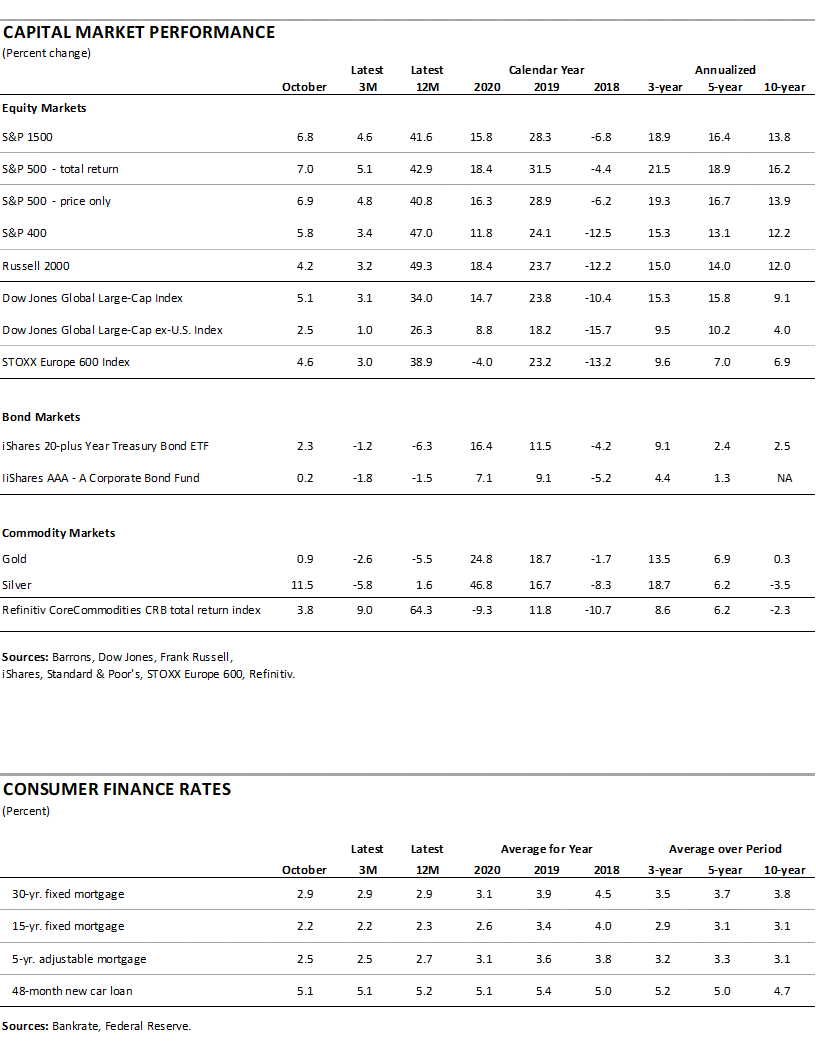

Summary

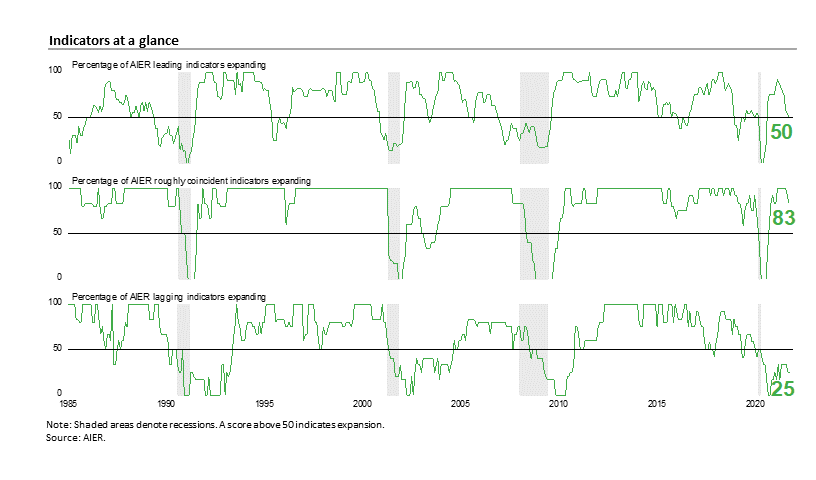

AIER’s Leading Indicators Index fell for a seventh consecutive month in October, hitting the neutral 50 mark. October was the weakest reading since August 2020. The Roughly Coincident Indicators Index fell for a second consecutive month while the Lagging Indicators Index was unchanged, remaining well below neutral. The string of declines in the Leading Indicators Index that began in April is consistent with the weak Gross Domestic Product report for the third quarter. Furthermore, the sagging performance suggests that risks remain elevated and that some caution is warranted. However, the neutral result for October is still a long way from signaling an elevated risk of recession, and the decline in new Covid cases is likely to allow activity to reaccelerate.

The Roughly Coincident Indicators index fell for the second consecutive month following a run of six consecutive months at 100. Despite the decline, the continued strength of the roughly coincident indicators remains a positive sign for the current expansion, but given the deteriorating strength of the Leading Indicators Index, some additional setbacks for the Roughly Coincident Indicators Index over the coming months would not be surprising. The Lagging Indicators Index remained at 25 in October and has been below the neutral 50 level for 18 consecutive months (see chart).

The now-fading resurgence in Covid cases was a significant headwind for the economy in the third quarter. The outbreak compounded difficult labor conditions, exacerbating shortages of materials and logistical issues. These conditions continued to exert upward pressure on prices. However, with new Covid cases now receding, businesses can refocus efforts on finding and hiring labor, expanding production, and easing supply chain difficulties. Such efforts are likely to be successful, leading to an easing of pressure on prices but it could take some time. Risks to the outlook remain elevated, but for now, continued economic expansion remains the likely path.

AIER Leading Indicators Index Fall to Neutral

The AIER Leading Indicators index posted a seventh consecutive decline in October, coming in at a neutral 50 reading versus 54 in September. The index is now down a total of 42 points over the last seven months from the recent high of 92 in March. October is the fourteenth consecutive month at or above the neutral 50 level, but it is also the lowest reading over that period and the lowest since August 2020 when the index was just 21. The neutral result suggests caution, but continued economic expansion remains the likely path.

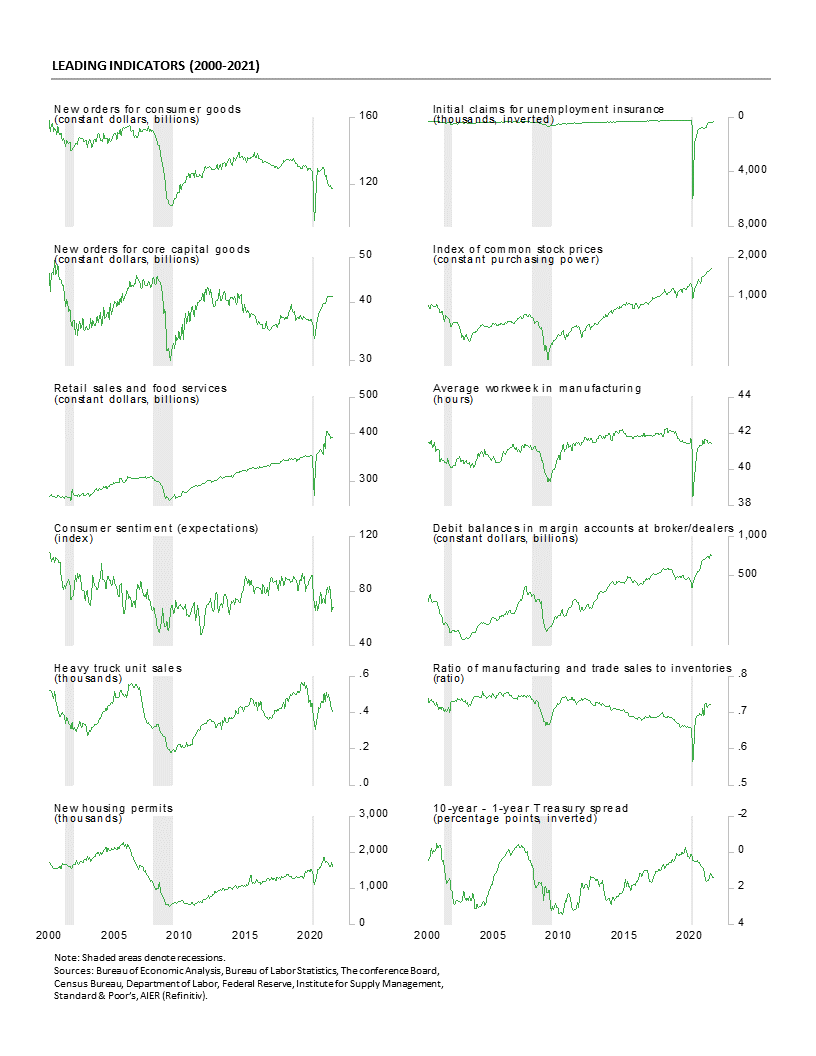

Among the 12 leading indicators, six were in a positive trend in October and six were trending lower with none trending flat or neutral. Just one of the 12 leading indicators changed direction in October. The average workweek in manufacturing turned from a neutral trend to a negative trend. The five other leading indicators with unfavorable trends are: the University of Michigan Index of Consumer Expectations, real new orders for consumer goods, total heavy truck unit sales, the Treasury yield spread, and housing permits. Initial claims for unemployment benefits, real retail sales, manufacturing and trade sales to inventory ratio, real new orders for core capital goods, stock prices, and debit balances in margin accounts were the six indicators maintaining favorable trends.

Overall, the Leading Indicators index posted another drop in October, coming in at the neutral 50 level. It was the fourteenth consecutive month at or above 50 but the lowest level over that period. Over the last 14 months, the leading indicators index has averaged 73.5 but the 42-point drop over the last seven months from the recent high of 92 in March is a troubling sign. The results suggest continued expansion is likely but the breadth of sources of growth could remain narrow in coming months and the pace of growth could remain weak.

However, the recent wave of new Covid cases has receded and should allow businesses to refocus on expanding production. Meanwhile, ongoing disruptions to labor supply and production, rising costs and shortages of materials, and logistics and transportation bottlenecks continue to exert upward pressure on prices. These issues are likely to be resolved over time and are unlikely to result in a 1970s-style price spiral, but the extended period of adjustment is likely to sustain a somewhat elevated level of risk for the economy.

The Roughly Coincident Indicators index fell nine points to 83 in October following a 92 result in September and six consecutive months at a perfect 100 reading from March through August. One indicator changed its signal in October as the Real Manufacturing and Trade Sales indicator fell from a neutral trend to a negative trend. Overall, five indicators were trending higher while one was trending lower, and none were in a neutral trend.

The Roughly Coincident Indicators index has been above the neutral 50 level for 13 consecutive months, posting an average reading of 90.4. The continued weakness in the Leading Indicator Index suggests some additional setbacks for the Roughly Coincident Indicators Index in coming months is possible. However, the decline in Covid cases may provide an offsetting boost.

AIER’s Lagging Indicators index remained at a weak reading of 25 in October. That was the 22nd consecutive month at or below neutral. The average over the last 22 months is 28.4. There were two offsetting changes in the latest month – Duration of unemployment improved from a negative trend to a neutral trend while Composite short-term interest rates fell from a neutral trend to a negative trend – leaving four indicators with unfavorable trends, one indicator with a favorable trend, and one in a neutral trend.

Economic growth slowed sharply in the third quarter, hampered by a wave of new Covid cases

Real gross domestic product increased at a 2.0 percent annualized rate in the third quarter, down sharply from a 6.7 percent pace in the second quarter and a 6.3 percent pace in the first quarter. Over the past four quarters, real gross domestic product is up 4.9 percent.

Real final sales to private domestic purchasers, a key measure of private domestic demand, rose at an even more disappointing 1.1 percent annualized rate in the third quarter following a 10.1 percent pace in the second quarter and 11.8 percent pace in the first quarter. Over the last four quarters, real final sales to private domestic purchasers are up 7.2 percent.

Weakness in the third quarter was concentrated in consumer spending but also seen in some components of business fixed investment and net trade. Real consumer spending overall rose at a 1.6 percent annualized rate, well below the strong 12.0 percent pace in the second quarter and 11.4 percent rate in the first quarter. Third quarter consumer spending contributed a total of 1.1 percentage points to real GDP growth versus a 7.9-point contribution in the second quarter.

Among the components of consumer spending in the third quarter, consumer services posted a 7.9 percent rate of growth, contributing 3.4 percentage points to growth, followed by nondurable goods with a 2.6 percent annualized growth rate (and adding 0.39 points to real GDP growth). Consumer durable-goods spending fell at a 26.2 percent pace, subtracting 2.7 percentage points from overall growth. Within consumer durable goods, spending was particularly weak on motor vehicles and parts which fell at a 53.9 percent annual rate and subtracted 2.4 percentage points from real GDP growth. The auto industry has been particularly hard hit by shortages of materials and components.

Business fixed investment increased at a 1.8 percent annualized rate in the third quarter of 2021, contributing 0.24 percentage points to final growth. However, that was below the 9.2 percent pace of growth in the second quarter (which added 1.21 percentage points to second quarter real GDP growth). Within the business fixed investment category, spending on equipment fell at a 3.2 percent pace (subtracting 0.18 points from growth) while spending on business structures fell at a 7.3 percent rate, the seventh decline in over the last eight quarters, subtracting 0.19 percentage points from final growth. Intellectual-property investment posted a 12.2 percent gain, adding 0.61 percentage points to final growth.

Residential investment, or housing, fell at a 7.7 percent annual rate in the third quarter compared to an 11.7 rate of decline in the prior quarter. The third quarter fall is the third decline in the last 6 quarters. The drop in the third quarter reduced overall growth by 0.38 percentage points. Housing had shown resilience throughout the pandemic as extremely low interest rates combined with widespread remote working policies and the desire by some people to move away from virus epicenters had supported increased demand. However, limited supply and surging home prices are pushing buyers out of the market, resulting in slower housing activity.

Businesses liquidated inventory at a $77.7 billion annual rate (in real terms) in the third quarter versus liquidation at a $168.5 billion rate in the fourth quarter, resulting in a 2.1 percentage point contribution to third-quarter growth.

Real exports fell at a 2.5 percent pace while real imports rose at a 6.0 percent rate. Since imports count as a negative in the calculation of gross domestic product, a gain in imports is a negative for GDP growth, subtracting 0.87 percentage points in the third quarter. The decline in exports subtracted 0.28 percentage points. Net trade, as used in the calculation of gross domestic product, subtracted a total of 1.14 percentage points from overall growth.

Government spending rose at a 0.8 percent annualized rate in the third quarter compared to a 2.0 percent pace of decline in the second quarter, adding 0.14 percentage points to final growth.

Demand Remained Strong for the Manufacturing Sector in October

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index fell to 60.8 in October, off 0.3 points from 61.1 percent in September. October is the 17th consecutive reading above the neutral 50 threshold and the eighth month above 60 in the last 11 months. The survey results suggest that the manufacturing sector continues to expand at a robust pace.

Among the key components of the survey, the New Orders Index posted a 6.9-point decline, coming in at 59.8 percent in October. The New Orders Index has been above 50 for 17 consecutive months but broke a string of 15 consecutive months above 60. The new export orders index, a separate measure from new orders, rose to 54.6 versus 53.4 in September. The new export orders index has been above 50 for 16 consecutive months.

The Production Index registered a 59.3 percent result in October, a decrease of 0.1 points in September. The index has been above 50 for 17 months.

The Employment Index rose in October, the second consecutive month above the neutral 50 level, to 52.0 percent. The index has been bouncing around between 49 and 53 for the last six months and may be reflecting the inability to hire rather than the lack of desire to hire.

The Backlog-of-Orders Index decreased in October, coming in at 63.6 versus 64.8 in September. This measure has pulled back from the record-high 70.6 result in May but has been above 50 for 16 consecutive months and above 60 for nine consecutive months. The index suggests manufacturers’ backlogs continue to rise at a rapid pace.

Customer inventories in October are still considered too low, with the index coming in at 31.7, unchanged from September (index results below 50 indicate customers’ inventories are too low). The index has been below 50 for 61 consecutive months. Insufficient inventory may be a positive sign for future production.

The index for prices for input materials moved back up in October, coming in at 85.7 percent versus 81.2 percent in September. While the index is down from a recent peak of 92.1 in June, it is still very high. Rising input costs have been driven by shortages of materials and labor as well as production issues and logistical and transportation problems. Those issues are reflected in the supplier deliveries index, which rose again in October to 75.6 from 73.4, suggesting deliveries slowed again in October.

Overall, demand for the manufacturing sector remains robust but labor difficulties, materials shortages, and logistical problems continue to hamper the ability to meet that demand. Many of these problems will ease over time, but the prolonged period of normalization will sustain upward pressure on prices and remain a threat to overall economic growth.

Core Capital-Goods Orders Suggest an Improving Outlook for Business Investment

New orders for durable goods fell in September, falling 0.4 percent, just the second decline in the last 17 months. Total durable-goods orders are up 20.7 percent from a year ago and 14.0 percent from January 2020. The September gain puts the level of total durable-goods orders at $261.3 billion, the third-highest level on record.

New orders for nondefense capital goods excluding aircraft or core capital goods, a proxy for business equipment investment, rose 0.8 percent in September after gaining 0.5 percent in August, 0.3 percent in July, and 1.0 percent in June, putting the level at $77.7 billion, another record high and the tenth new high in the last eleven months. Core capital-goods orders had broken the $70 billion mark only once before, in February 2012, but have been above $70 billion for 11 consecutive months.

Among the categories in the report, gainers outnumbered decliners four to three. Among the individual categories, primary metals rose 0.6 percent, fabricated metal products gained 0.7 percent, machinery orders increased by 1.1 percent, and the catch-all “other durables” category added 0.3 percent while computers and electronic products fell 0.3 percent, electrical equipment and appliances were off 0.5 percent, and transportation equipment sank 2.3 percent. Within the transportation equipment category, motor vehicles and parts dropped 2.9 percent as auto manufacturers grappled with ongoing chip shortages, nondefense aircraft lost 27.9 percent, but defense aircraft surged 104.3 percent. From a year ago, every category shows a gain. Likewise, comparing the latest results to pre-pandemic levels, every category shows a gain with all but one posting double-digit growth.

Durable-goods orders continue to run at a high level, particularly the core-capital goods components. Demand remains strong for the manufacturing sector, and the tight labor market creates incentives to substitute capital for labor. The pandemic may be accelerating structural changes to the economy, affecting labor, housing, manufacturing, and services. With the decline of the recent resurgence of new Covid, the outlook for growth is once again strengthening. However, upward pressure on prices continues as demand outpaces supply. As labor, materials, and logistical issues are alleviated, price pressures are likely to ease, but the process may take a significant period of time.

Lingering Effects from Covid and Hurricane Ida Hurt Industrial Output in September

Industrial production fell 1.3 percent in September, the second decline in a row and the largest monthly drop since February. The decline pushed total output back below the February 2020 level. Over the past year, total industrial output is still up 4.6 percent. Much of the decline was accounted for by the lingering effects of Covid which has been causing disruptions to manufacturing (especially motor vehicles production), and the effects of Hurricane Ida (about 0.6 percentage points of the 1.3 percent decline) which shut down significant portions of activity in the coastal region along the Gulf of Mexico, especially for the energy industry.

Capacity utilization fell a full percentage point to 75.2 percent from 76.2 percent in August and is below the February 2020 level of 76.3 percent. Total capacity utilization is also well below the long-term (1972 through 2020) average of 79.6 percent.

Manufacturing output – about 76 percent of total output – posted a 0.7 percent decrease for the month, the second decline in a row and the fourth drop in the last seven months. Manufacturing output is still above its February 2020 level and is up 4.8 percent from a year ago. Effects of Hurricane Ida accounted for about 0.3 percentage points of the 0.7 percent drop in manufacturing.

Manufacturing utilization fell 0.6 points to 75.9 percent but remains above the February 2020 level of 75.5 percent. However, manufacturing utilization remains below its long-term average of 78.2 percent and well below the 1994-95 high of 84.7 percent.

Mining output accounts for about 12 percent of total industrial output and posted a sharp 2.3 percent decrease last month. Over the last 12 months, mining output is up 6.9 percent. The lingering effects of Hurricane Ida more than accounted for the drop in mining activity.

Utility output, which is typically related to weather patterns and is also about 12 percent of total industrial output, decreased 3.6 percent for the month. From a year ago, utility output is up 1.6 percent.

Among the key segments of industrial output, energy production (about 25 percent of total output) fell 3.1 percent for the month with declines in all five components. Total energy production is still up 4.8 percent from a year ago.

Motor-vehicle production (about 5 percent of total output), one of the hardest-hit industries during the lockdowns, continues to be volatile as the industry struggles with a semiconductor chip shortage. Motor-vehicle production sank 7.2 percent in September following a 3.2 percent drop in August and is down in five of the last eight months. From a year ago, vehicle production is off 13.7 percent. Total vehicle assemblies fell to 8.60 million at a seasonally-adjusted annual rate. That consists of 8.33 million light vehicles and 0.27 million heavy trucks. Within light vehicles, light trucks were 7.18 million while cars were 1.41 million.

The selected high-tech industries index rose 0.6 percent in September and is up 10.7 percent versus a year ago. High-tech industries account for just 2.2 percent of total industrial output.

All other industries combined (total excluding energy, high-tech, and motor vehicles; about 68 percent of total industrial output) fell 0.2 percent in September but are 5.9 percent above September 2020.

Industrial output showed broad weakness in September, hurt by the lingering effects of Covid that has resulted in shortages of materials, and the lingering effects of Hurricane Ida that hit the energy industry particularly hard. While ongoing difficulties with labor, logistics, and materials shortages continue to be challenges for many industries especially in manufacturing, some of these issues may start to ease in the coming months and quarters, helping to reduce some of the upward pressure on prices.

Overall Outlook: Risks ease but remain elevated as Covid recedes but labor difficulties and shortages sustain upward pressure on prices

The AIER Leading Indicators index posted a seventh consecutive drop in October, coming in at a neutral 50 versus 54 in September. The October result suggests continued economic expansion but the string of declines since the March high also suggest that sources of growth may remain narrow. However, the decline in new Covid cases may provide a boost as businesses reaccelerate efforts to attract labor and boost production.

The Roughly Coincident Indicators index also fell in October but has been at or above the neutral 50 level for 13 consecutive months. The solid performance of the Roughly Coincident Indicators index since the government-induced recession of 2020 reflects the broad-based economic recovery, but the continued weakness in the Leading Indicator Index suggests some additional setbacks in coming months are possible.

AIER’s Lagging Indicators index remained weak, coming in well below neutral again in October. The latest result was the 22nd consecutive month at or below neutral.

The decline in the recent surge in new cases should allow businesses to reaccelerate efforts to attract labor and boost production. However, ongoing labor difficulties (including a lack of qualified workers, absenteeism, temporary shutdowns, and inability to retain talent), materials shortages, and logistical and transportation bottlenecks are sustaining upward pressure on prices (though a 1970s-style price spiral remains unlikely). The outlook is for continued economic expansion, though the risks to growth remain somewhat elevated. A moderate level of caution remains warranted.

0 Comments