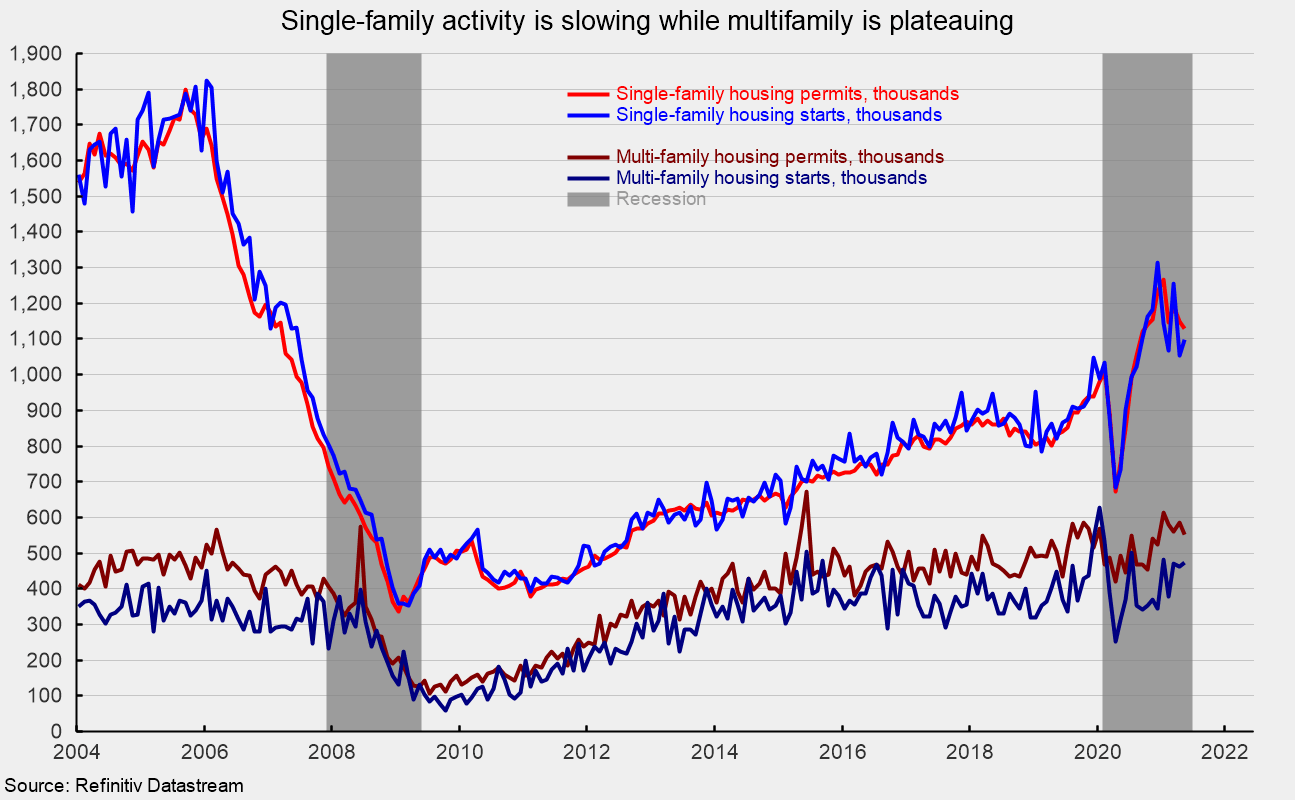

Total housing starts rose to a 1.572 million annual rate in May from a 1.517 million pace in April, a 3.6 percent increase. From a year ago, total starts are up 50.3 percent. However, total housing permits fell 3.0 percent to 1.681 million in May from 1.733 million in April. Total permits are 34.9 percent above the May 2020 level. Both continue to trend down from peaks around the start of the year.

The dominant single-family segment saw starts rise 4.2 percent for the month to a rate of 1.098 million and are up 49.8 percent from a year ago. Single-family permits however were off 1.6 percent at 1.130 million. Single-family starts and permits are also trending lower from peaks around the start of the year (see first chart).

Starts of multifamily structures with five or more units rose 4.0 percent to 465,000 and are up 52.5 percent over the past year but starts for the two- to four-family-unit segment plunged 43.8 percent to 9,000. Combined, multifamily starts were up 2.4 percent to 474,000 in May (see first chart).

Multifamily permits for the 5-or-more group fell 7.7 percent to 494,000 while permits for the two-to-four-unit category rose 14.0 percent to 57,000. Combined, multifamily permits were 551,000, down 5.8 percent for the month. Multifamily permits may be plateauing or starting to trend lower (see first chart).

Single-family home construction had been one of the strongest parts of the economy last year and excluding the plunge in activity during the government-enforced lockdowns in early 2020, single-family housing activity has been on an upswing for most of the last decade, recovering from the housing bubble and collapse of the late 2000s (see first chart). The post-lockdown recovery has been supported by a surge in demand as consumers sought less dense housing. However, since December, single-family activity has been trending lower. It may be that some of the rush to less dense housing that drove the single-family surge in activity in the second half of 2020 is starting to ease as the economy opens, more people get vaccinated, and workers return to offices.

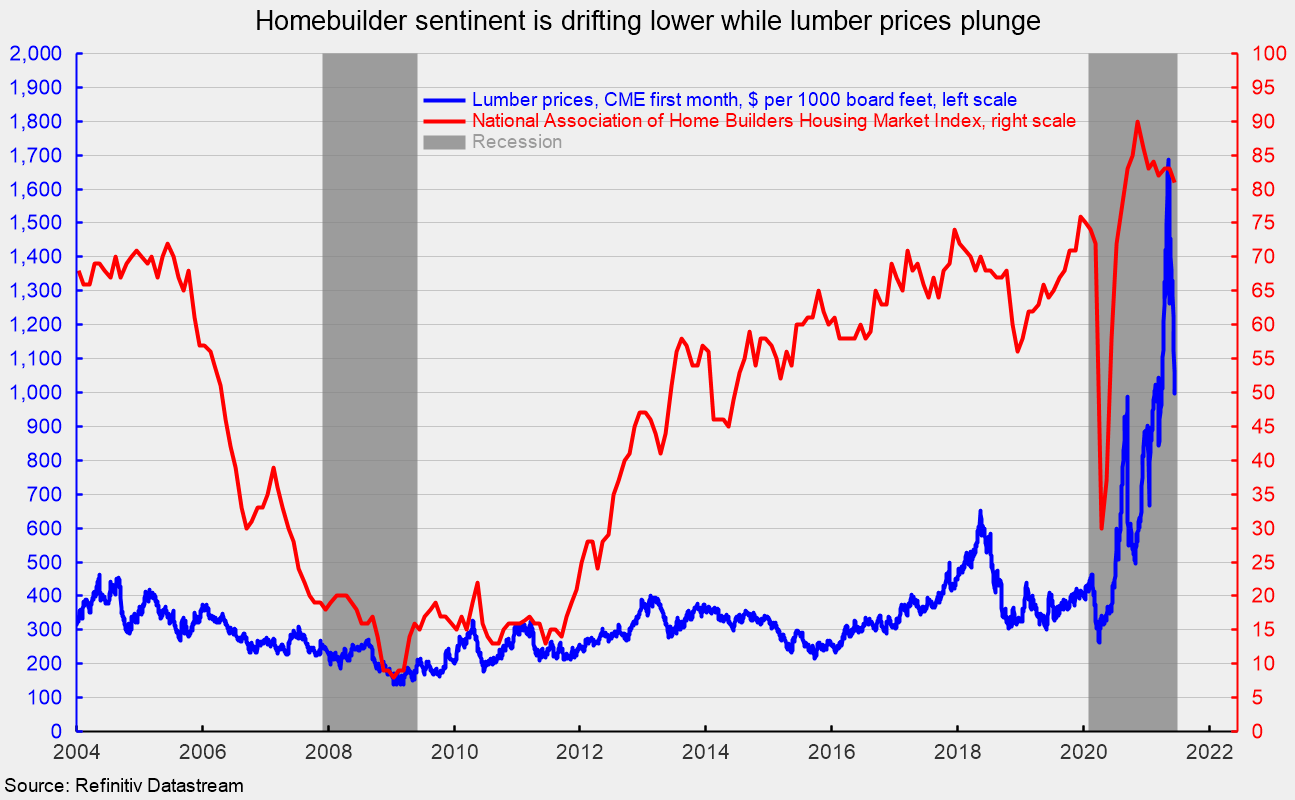

Similarly, the surge in demand that sent lumber prices soaring has reversed course in recent weeks as sales and construction show signs of cooling. Lumber prices peaked around $1,700 per 1,000 board feet and are currently around $1,000, a drop of about 40 percent. However, that is still well above the $300 to $500 range of 2019 (see second chart).

Furthermore, the National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell again in June, to 81 from 83 in May and a peak of 90 in November 2020 (see second chart). Overall sentiment remains relatively high but elevated materials costs are pushing prices up and forcing some buyers out of the market, resulting in lower demand.

All three components of the Housing Market Index fell in June. The current single-family sales index fell to 86 from 88 in the prior month, the expected single-family sales index fell to 79 from 81, and the traffic of prospective buyers index was off two points to 71.

Housing may have enough momentum to grow at a solid pace in 2021 but the combination of a reopening economy and rapidly rising home prices will likely lead to some cooling. For the homebuilders, fundamentals remain sound but rising materials costs and labor difficulties are creating challenges.

0 Comments