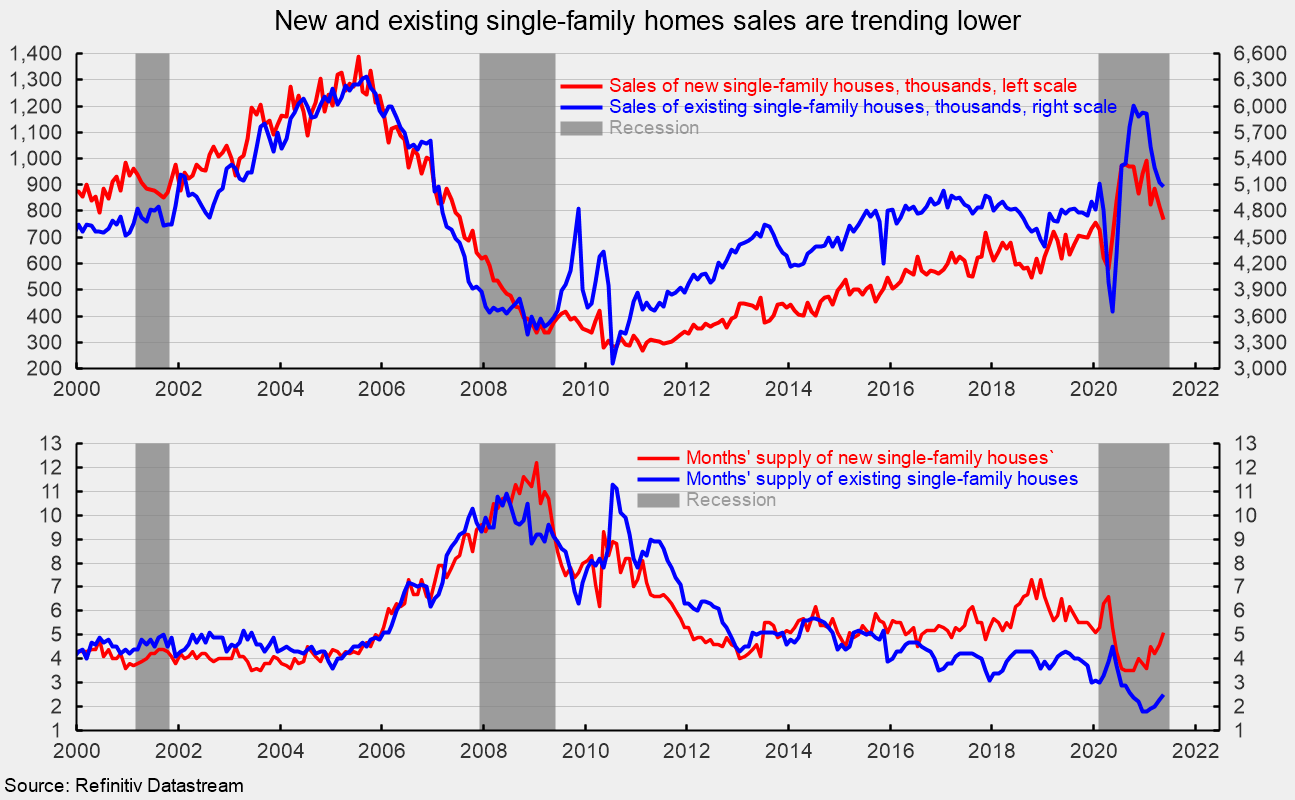

Sales of new single-family homes fell sharply in May, decreasing 5.9 percent to 769,000 at a seasonally-adjusted annual rate from a 817,000 pace in April. Sales are still up 9.2 percent from the year-ago level but are well below the 993,000 pace in January (see top of first chart). Weakness over the last few months in sales of new single-family homes is consistent with signs of slowing in the market for existing single-family homes as well (see top of first chart).

Sales of new single-family homes were down in just one of the four regions of the country in May with declines in the South, the largest by volume, off 14.5 percent for the month. Sales were unchanged at 95,000 in the Midwest and up 33.3 percent in the Northeast and 6.7 percent in the West. From a year ago, sales are still up in all four regions: 57.6 percent in the Northeast, 28.4 percent in the Midwest, 6.7 percent in the West, and 3.1 percent in the South.

The total inventory of new single-family homes for sale rose 4.8 percent to 330,000 in May, the highest level since May 2019, leaving the months’ supply (inventory times 12 divided by the annual selling rate) at 5.1, up 10.9 percent from April but 3.8 percent below the year-ago level (see bottom of first chart). The median time on the market for a new home fell in May, coming in at 3.5 months versus 4.5 in April.

Recent headwinds for the housing market include somewhat higher mortgage rates and sharply higher home prices. The average rate of a 30-year fixed-rate conforming mortgage was 2.96 percent in May, down from 3.06 in April but up from a low of 2.68 in December. The median sales price of a new single-family home was $374,400 (see top of second chart), an 18.1 percent gain from a year ago (see bottom of second chart).

The combination of high prices and rising mortgage rates is forcing some buyers out of the market and contributing to a slowing in housing activity. It is likely that these conditions will continue to significantly impact the overall housing market, further reducing demand, easing the tight supply, and slowing future price increases.

0 Comments