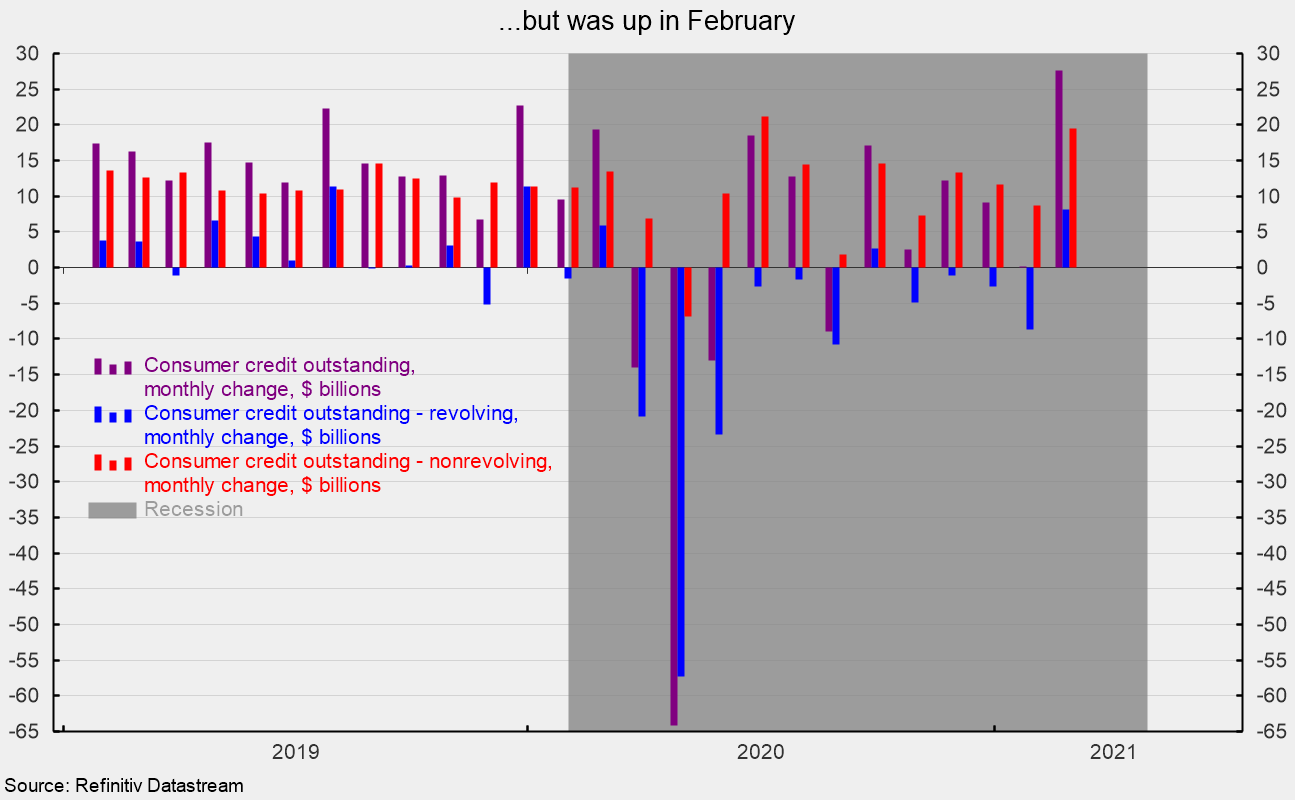

Total consumer credit outstanding rose $330.9 billion at an annual rate to $4,205.8 billion in February (see top of first chart), a 7.9 percent increase from the prior month. From a year ago, total consumer credit is unchanged (see bottom of first chart), well below the 25-year annualized pace of 5.3 percent. Within the total, revolving credit, primarily credit cards, totaled $974.4 billion (see top of first chart), an 11.2 percent decline over the past year (see bottom of first chart), while nonrevolving credit was $3,231.4 billion (see top of first chart), a 4 percent gain from a year ago (see bottom of second chart).

While revolving credit outstanding is down from a year ago, the category rose at a $97.1 billion annual rate in February (see second chart), or 10.1 percent from the prior month. That was the largest monthly gain since December 2019 and follows declines in 10 of the past 11 months.

Total nonrevolving credit outstanding rose at a $233.8 billion annual rate in February, 7.3 percent above the January pace. That was the largest gain since June 2020.

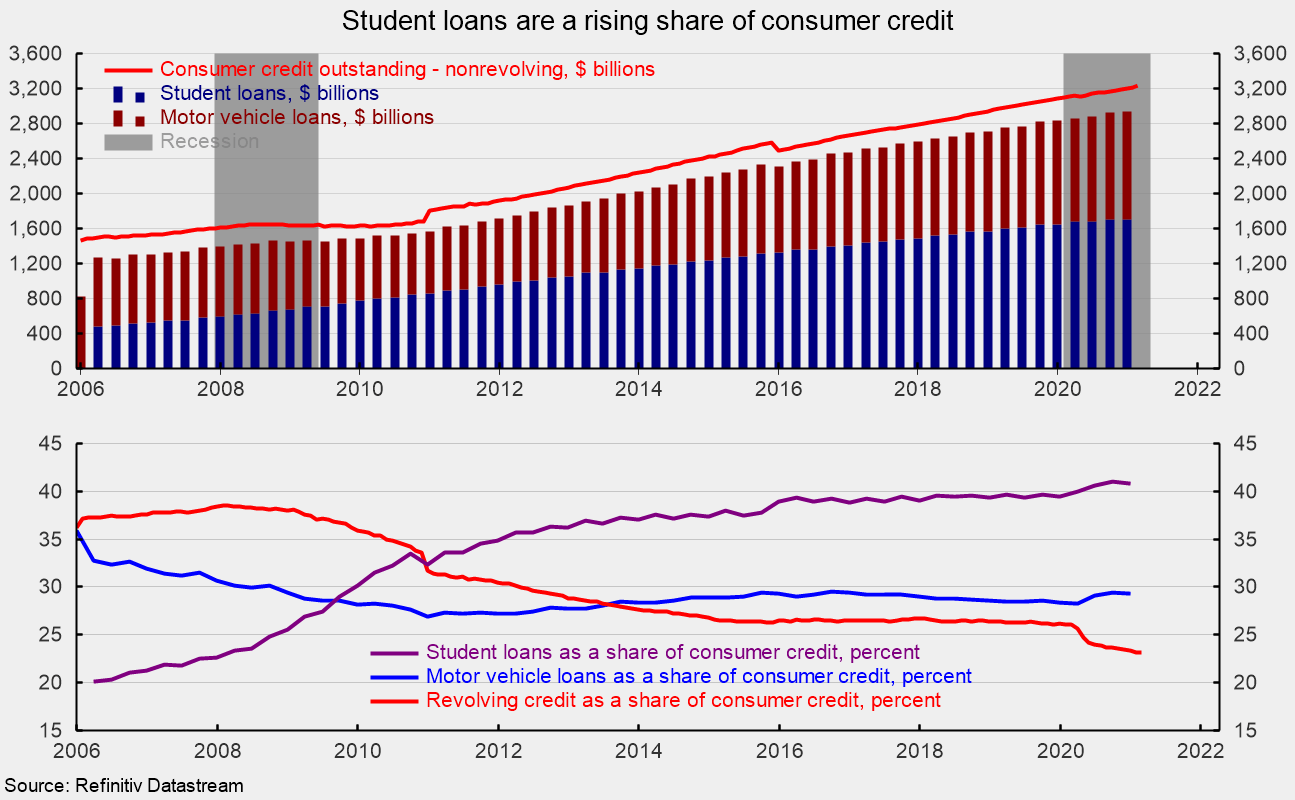

Nonrevolving credit has been growing rapidly over the past decade and a half, driven primarily by student loans and motor vehicle loans. As of the end of the fourth quarter, student loans totaled $1,707.3 billion, or 53.3 percent, and auto loans totaled $1,225.1 billion, or 38.2 percent. Together, they account for 91.5 percent of nonrevolving debt outstanding and 70.2 percent of total consumer credit. Revolving consumer credit was just 23.2 percent of total consumer credit as of February 2021.

Total consumer credit jumped in February on gains in revolving credit and nonrevolving credit. The gain in revolving credit goes against the recent trend while nonrevolving credit continued the strong growth trend. The lingering distortions of lockdowns on consumer spending, consumer credit usage, and personal saving may continue for several months. While aggregate numbers suggest a positive outlook (high levels of savings could lead to strong spending as pent up demand is satisfied), the effects of the lockdowns vary widely across industries and cohorts of consumers.

0 Comments